ASEAN countries are characterized by considerable diversity but share an outward-oriented development strategy. While intra-regional economic cooperation over the past two decades has been important, global, not regional, interaction has been the key to ASEAN’s success story. Hence, the strong policy headwinds facing globalization in the post-Covid period threaten continued growth and prosperity in the region. Proposals in major markets to protect domestic industries by raising obstacles to trade vary from sectoral protection to more comprehensive “geopolitical” or “geoeconomic” approaches, such as: (1) re-shoring to encourage local production; (2) near-shoring to encourage trade with regional partners; and (3) friend-shoring to support trade with political and diplomatic allies at the expense of others. The result could be “geoeconomic fragmentation” (Aiyar, et. al., 2023).

These fragmentation scenarios would leave ASEAN economies particularly exposed. Re-shoring negatively affects small, open economies the most. The large share of extra-regional markets for its exports makes ASEAN vulnerable to near-shoring, and as a basically non-aligned region, its members could well be excluded as “friends” from key markets. One goal of the paper on which this post is based, Petri and Plummer (2023), is to estimate what effects these global scenarios would have on ASEAN incomes, trade, and participation in global value chains (GVCs).

A second question the paper addresses involves ASEAN policy: Can wider economic cooperation through enlargement of the Comprehensive and Progressive Agreement for Transpacific Partnership (CPTPP) and the Regional Comprehensive Economic Partnership (RCEP) serve as a bulwark against the New Protectionism? The paper estimates the potential economic effects of RCEP itself which went into effect in January 2022, two prospective expansions of the CPTPP, and a “global reach” scenario which would include further expansion of the CPTPP and RCEP.

The paper uses a new Computable General Equilibrium model based on the World Trade Organization’s Global Trade Model to estimate the effects of geopolitical restructuring and economic cooperation scenarios with a focus on the ASEAN economies, and then traces the implications for their participation in GVCs via a Multi-Regional Input-Output subsystem.

Geoeconomic Fragmentation

In our simulations, all three geoeconomic fragmentation scenarios are implemented with barriers (represented by tariffs) that restrict trade in line with scenario objectives. The scenarios are defined as follows. (1) Re-shoring: large economies apply protection levels of 7.5 percent to general imports and 15 percent to sensitive imports. (2) Near-shoring: seven regional blocs apply protection levels as in (1) on all extra-regional trade. (3) Friend-shoring: the United States and China construct blocks with their close allies, applying protection levels as in (1) between blocs, with regions not included in either bloc facing half the tariffs as opposing bloc members.

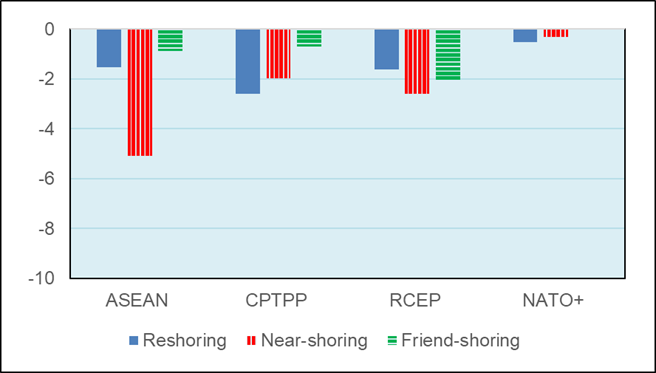

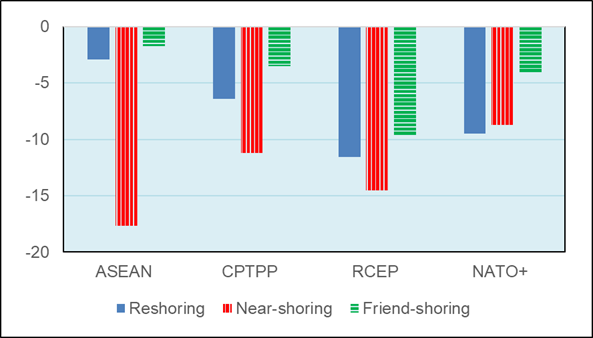

For each geoeconomic intervention, the results for selective organizations, including ASEAN (10)1, CPTPP (11)2, RCEP (15)3, and NATO+4, are summarized in Figure 1 for changes in real income and exports through 2035. As anticipated, open developing economies like those in ASEAN are the most vulnerable to these shocks, especially near-shoring given that their export markets are global rather than regional: ASEAN real incomes contract by about 5 percent whereas global incomes decline by about 1 percent. Trade contracts significantly for all country groupings. Near-shoring is particularly damaging to Asian economies: ASEAN trade contacts by about 18 percent and RCEP trade by about 15 percent.

|

Figure 1. Geopolitical Interventions |

|

Economic Cooperation

In our simulations, we consider four possible economic cooperation scenarios: (1) RCEP, which began implementation in January 2022 and is not in the baseline; (2) a first enlargement of the CPTPP (CPTPP2) in 2024, which envisions the entry into force for the CPTPP countries that had not yet ratified the CPTPP by 2022 together with the United Kingdom and South Korea5; (3) a second enlargement of the CPTPP in 2027, to include three ASEAN economies—Indonesia, the Philippines and Thailand—that have expressed interest in joining the group; and (4) a “global reach” scenario, used as a globalization benchmark rather than a prediction, to include China, the United States, the European Union, and Taiwan.6

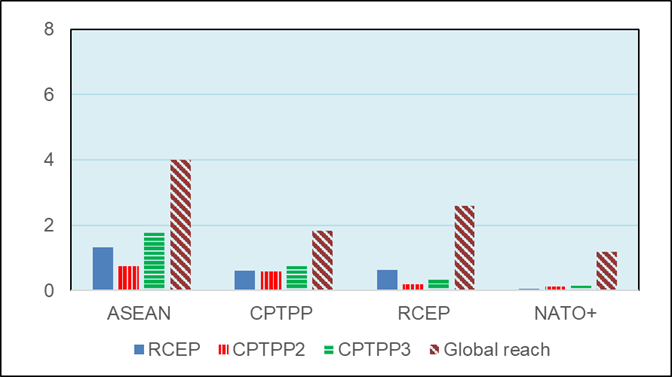

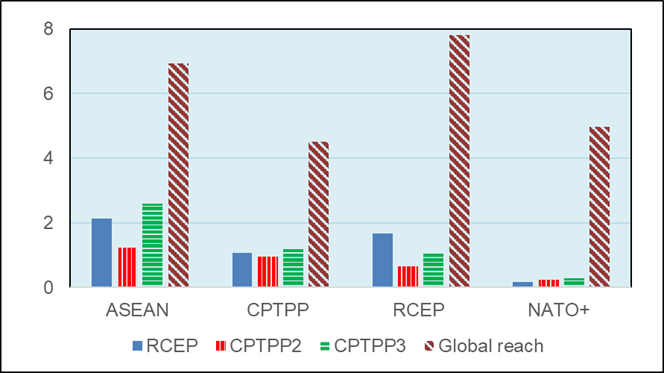

Results are presented in Figure 2 for changes in real income and exports. ASEAN economies gain significantly from RCEP, with real incomes rising by about 1.5 percent on average relative to the baseline, despite the fact that the region already had in place free-trade areas with all non-ASEAN RCEP members. CPTPP2 and CPTPP3 increase regional income gains by almost 2 percent. Hence, in general, the overall value of the CPTPP and its enlargements are on par with that of RCEP. Exports increase by more than income in all scenarios.

The “global reach” scenario would generate gains many times those of RCEP and the CPTPP enlargements. In fact, the agreement would add annually $1.4 trillion and $1.6 trillion to global incomes and international trade, respectively, by 2035. The real incomes of members would expand by 1.6 percent, with China, the United States and Europe appearing as the biggest beneficiaries. ASEAN economies would see their real incomes and exports rise by 4 percent and 7 percent, respectively. Of course, this scenario seems particularly implausible these days in light of the trade conflict between the United States and China. Still, what is implausible today may not be so in the future.

|

Figure 2. Economic Cooperation Scenarios |

|

Implications for GVCs

In terms of the effects on GVCs, the fact that products cross borders multiple times suggests that they are unusually sensitive to changes in trade policy. In our estimates, geoeconomic fragmentation reduces the share of GVCs in trade by 5-9 percent relative to the baseline, depending on the scenario. While some ASEAN economies are only marginally affected by re-shoring with a regional average drop of 2.6 percent, as expected the negative effect from friend-shoring is large, in the range of -8 percent to -12 percent for ASEAN economies and a regional average drop of 9.2 percent. Economic cooperation scenarios raise GVC participation but by much less than the negative effects of geoeconomic fragmentation: world (ASEAN) aggregates rise by 0.5 percent (0.3 percent) under RCEP; 0.4 percent (0.3 percent) under CPTPP3; and 2.3 percent (0.6 percent) under global reach.

Conclusion

ASEAN is deeply integrated into the global economy and, hence, its prospects for growth and prosperity are a function of trends in global commercial policy. Therefore, the current protectionist zeitgeist is of great concern to ASEAN policymakers. Our simulations suggest that geoeconomic fragmentation in the form of re-shoring, near-shoring, and friend-shoring could have very negative ramifications for ASEAN’s trade prospects and its participation in GVCs and, hence, its future growth. Outward-looking economic cooperation will in part offset the effects of the New Protectionism. However, the region will continue to be vulnerable to the fragmentation of global markets.

The policy lessons are clear: the region should continue to work with its allies to keep international markets open, strengthen global trade governance, and promote outward-oriented regional economic cooperation.

_____________________________

1 Brunei Darussalam, Cambodia, Indonesia, Lao PDR, Malaysia, Myanmar, the Philippines, Thailand, Singapore, and Vietnam.

2 Australia, Brunei Darussalam, Canada, Chile, Japan, Mexico, Malaysia, New Zealand, Peru, Singapore, and Vietnam.

3 ASEAN countries plus Australia, China, Japan, New Zealand, and South Korea.

4 Australia, Canada, Europe, Japan, New Zealand, South Korea, United Kingdom, and United States.

5 Malaysia and Chile both ratified the agreement at the end of 2022 and the United Kingdom will likely sign the CPTPP in summer 2023. In April 2022 South Korea expressed its intention to join the CPTPP.

6 Both China and Taiwan have formally applied to join the CPTPP.