Co-authors: John R. Birge; Zi'ang Wang; Jing Wu

This post draws from a paper to be presented in the ACAES session on Asian Economies in Global Supply Chains at the 2023 Allied Social Science Association Annual Meeting, program here.

The vulnerability of global supply chains and their impact on the economy has become a central issue during the current COVID-19 pandemic. While global supply chains allow firms to outsource production more cost effectively, they also expose firms to developments in the local economies where supply chain partners are located. During the recent COVID-19 pandemic, countries took measures to contain the pandemic through shutdowns and social distancing mandates. These measures created disruptions for local firms and their supply chain partners located in different regions. Disruptions in supply chains adversely affected production for downstream firms, and financial flows for upstream firms, creating major vulnerabilities for firms connected within a production network.

Examining U.S. firms’ supply chain relations to China during the COVID-19 pandemic provides important insights on the credit risk implications of global supply chains. There are several reasons why focusing on China is important. First, China is a major production center in the world, providing components, materials, and subsystems to companies globally. Second, among U.S. trade partners, China is the largest source of imports, providing 18% of total U.S. imports in 2019. Thus, COVID-19 related economic disruptions in China have significant potential consequences for U.S. firms. Finally, China experienced different phases of COVID-19 earlier than the rest of the world, which allows understanding of the implications of supply chain disruptions and resumptions in a less confounded setting.

There were two distinct periods in regard to supply chain disruptions and resumptions in China in the early stages of the pandemic: (1) when the Chinese economy shut down due to COVID-19 (January 31–February 29, 2020), which also corresponds to the time period right after the U.S. banned travel to China on January 31 (refereed to as Phase 1 here); (2) when the Chinese economy reopened, and production resumed once the pandemic was under control (March 1- April 6, 2020) (referred to as Phase 2 here). During Phase 1, COVID-19 spread and the Chinese economy slowed down. During Phase 2, the Chinese economy re-opened as COVID-19 infections were under control whereas the pandemic then spread globally, adversely affecting the U.S. through stay-at-home orders and economic slowdown.

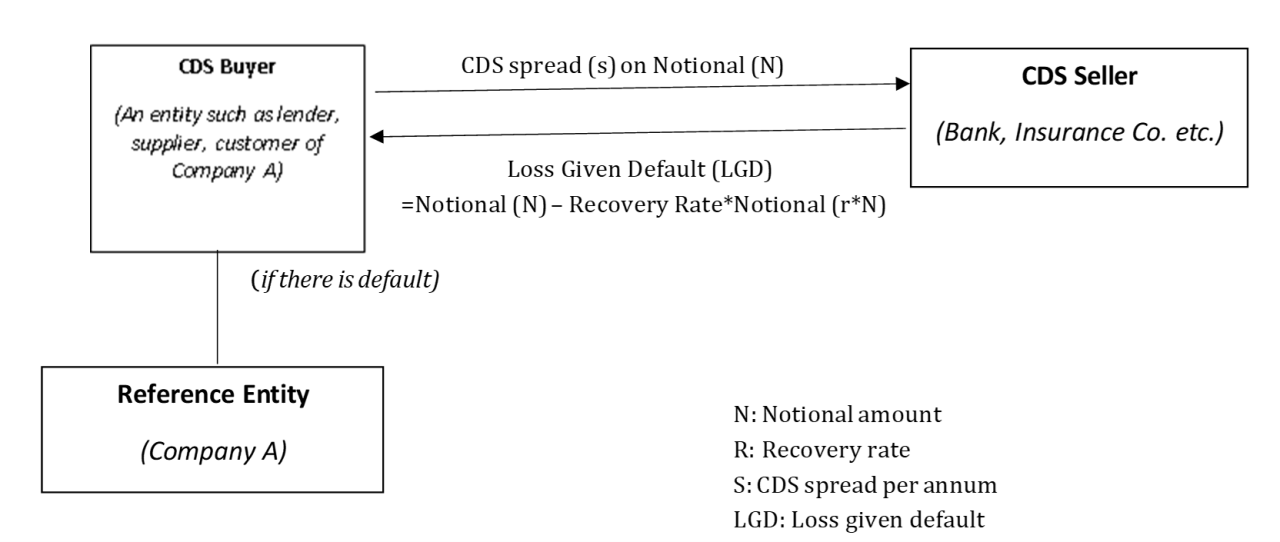

Credit default swaps (CDS) are used to examine credit risk of U.S. firms with Chinese supply chain partners. CDS contracts are financial contracts that protect the buyer when there is a default. Thus, developments in the CDS markets provide a gauge of credit risk that firms face from supply chain disruptions resulting from COVID-19. Abnormal CDS spreads are calculated by deducting industry and rating-adjusted CDS index spread from the CDS spread of each firm at each date as depicted in Figure 1.

|

Figure 1. Calculation of Abnormal CDS Spreads |

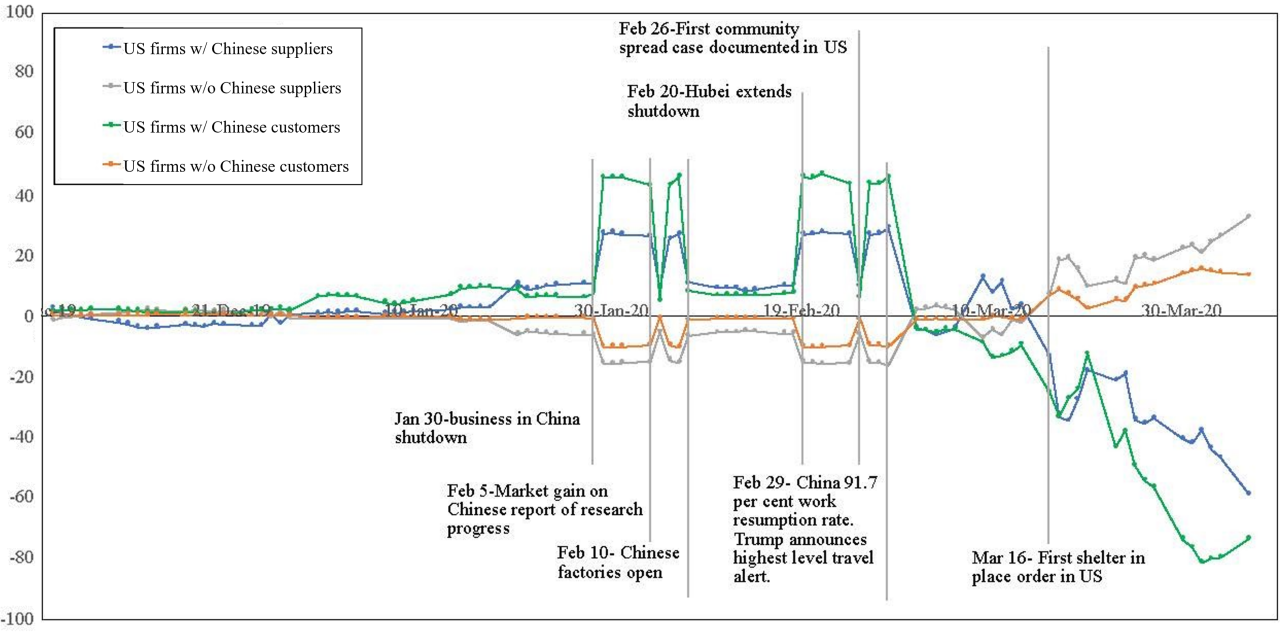

Results presented in Figure 2 show that during Phase 1 - the period of economic shutdown in China, abnormal CDS spreads went up considerably for U.S. firms with supply chain partners in China. Such increases in abnormal CDS spreads were observed for U.S. firms with Chinese suppliers as well as for those with Chinese customers. During Phase 2 - when economic activity in China resumed, abnormal CDS spreads of U.S. firms with Chinese suppliers or customers declined significantly, indicating reduced default risk with supply chain activity resumption.

|

Figure 2. Abnormal CDS Spreads for U.S. Firms with Supply Chains in China, Dec 2019 to Mar 2020

|

Closer examination shows abnormal CDS spreads for U.S. firms with suppliers in China increased by 21 basis points (bps) in Phase 1 and decreased by 24 bps in Phase 2. For U.S. firms with customers in China, the corresponding values were a 26 bps increase in Phase 1 and a 40 bps decrease in Phase 2. These changes correspond to increases of around 12 to 14 percent in CDS spreads on average in Phase 1, and decreases of about 8 to 11 percent on average in Phase 2. Thus, average CDS spreads of U.S. firms increased substantially in Phase 1 when the Chinese economy shut down, and supply chains were disrupted as a result. The resumption of supply chain activities in China in Phase 2 improved credit risk for U.S. firms with Chinese supply chain partners considerably. During Phase 2, China was in the economic recovery phase whereas the pandemic was spreading to create global disruption. Therefore, supply chain links to China proved advantageous for U.S. firms during Phase 2.

When sector breakdowns are considered, those sectors more closely connected to household demand, such as consumer goods and electronics, were found to respond not only to supply chain disruptions but also to household demand effects on the U.S. domestic economy. Declining domestic demand in the U.S. in Phase 2 due to economic shutdowns adversely affected firms more closely related to consumers. However, during this period, U.S. firms with a customer base in China showed a better credit risk profile as the Chinese economy was operating at normal levels. Thus having a global customer base helped to mitigate the impact of local shocks when supply chain vulnerabilities resolved.

Further analysis shows vulnerability to supply chain disruptions increases with higher financial and operational leverage and with exposure to more competitive markets. Since high financial leverage raises the likelihood of default and high operating leverage limits the ability to adjust operating costs, firms that face these conditions are more sensitive to supply chain developments. Firms in highly competitive markets face potential substitution by buyers, which increases supply chain vulnerabilities. Firms show stronger supply chain resilience in connection with larger size, investment grade rating, and greater cash and inventory balances. Firms that are more centrally located in production networks also have stronger resilience to supply chain developments. Lenders may prefer larger firms due to their ability to provide asset collateral, and investment-grade companies are far from the default boundary. Thus, these firms are able to withstand adverse developments. Companies with higher cash levels and greater inventory have better cushioning. Firms that are central in production networks have a more ability to hedge across multiple supply chains, reducing their sensitivity to supply chain disruptions.

Overall, during the COVID-19 pandemic, disruptions and resumptions in both local and global supply chains were reflected in credit risk as measured in CDS spreads. CDS markets reveal this risk dissemination arising from changing supply chain dynamics. Specific factors that increase supply chain resilience include lower financial and operating leverage, higher cash and inventory balances, and a more central position in the supply chain network to diversify risk. For managers, these key factors can be used as a basis for risk assessment in anticipation of disruptions.

_______________________

Co-author John R. Birge is a Professor at the University of Chicago Booth School of Business.

Co-author Zi'ang Wang is Research Assistant Professor at the CUHK Business School, Chinese University of Hong Kong.

Co-author Jing Wu is Associate Professor at the CUHK Business School, Chinese University of Hong Kong.