Co-Authors: Peter A. Petri; Fan Zhai

In December 2015 the ASEAN Economic Community (AEC) went into effect. It was the culmination of a process that began with the Bangkok Declaration in 1967 and represents the most significant economic integration initiative among developing economies in the world. A notable milestone to be sure, but the region has a long way to go before it will be able to attain its original goal of creating a 21st century single market and production base. Meanwhile, ASEAN needs to nest the next stage of its cooperation program in the context of emerging megaregional trade arrangements, namely, the Comprehensive and Progressive Agreement on Trans-Pacific Partnership (CPTPP) and the Regional Comprehensive Economic Partnership (RCEP), and the future expansions of both. In addition, it has to do this at a challenging time for the global trading system upon which it depends; the US-China trade war continues with no clear resolution on the horizon, the World Trade Organisation is at an impasse, and the Covid-19 pandemic has decimated global trade in the short run and may have long-term implications (UNCTAD 2020).

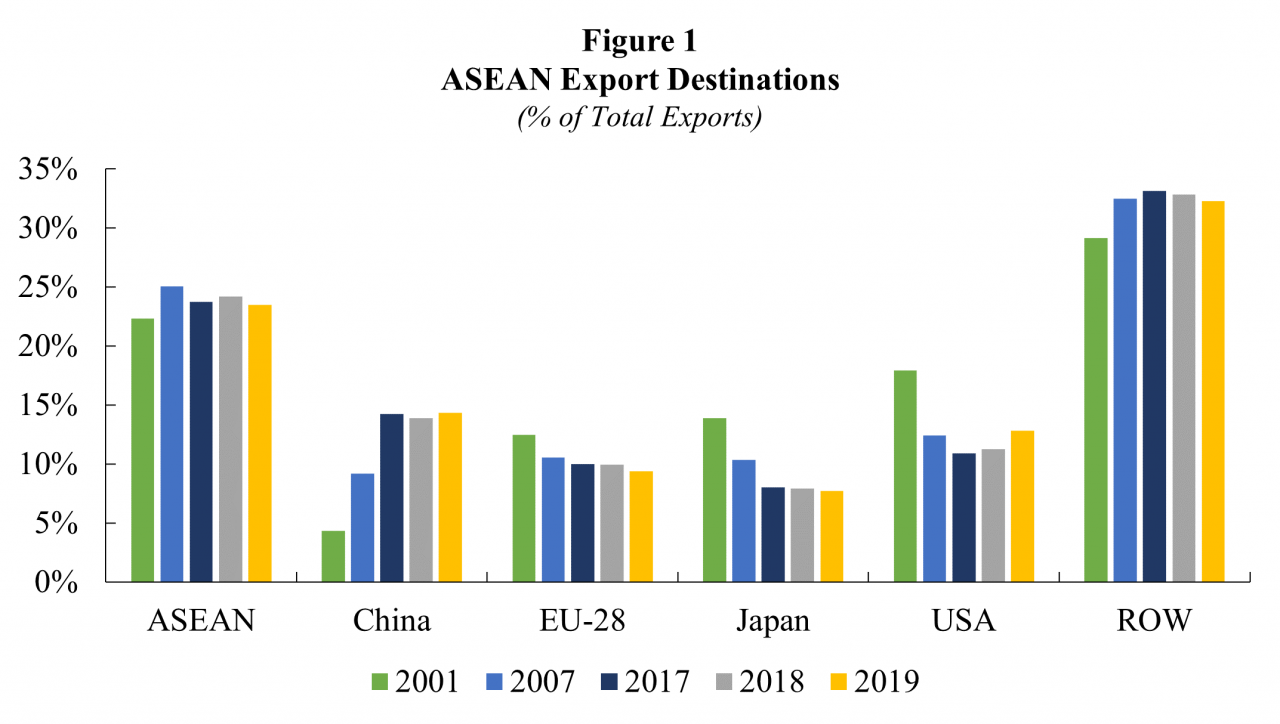

The AEC is arguably a crucial step in the development of an integrated Asia-Pacific regional economy. ASEAN cooperation dates back more than a half-century, but it was really the ASEAN Free-trade Area (AFTA) in 1992 that started the region on the path toward deep integration (Petri and Plummer 2014). It subsequently negotiated a series of “ASEAN+1” agreements with trading partners. In 2002, ASEAN leaders committed to the creation of the AEC by 2020, moved up to 2015 via the Cebu Declaration of 2007. The economic effects were expected to be large. For example, using a Computable General Equilibrium (CGE) model, Petri, et. al. (2012) estimated that the AEC would lead to an increase in regional income by 5.3 percent on a permanent basis beginning in 2025. Nevertheless, the AEC project is definitely a work in progress and, while AFTA is in place, much remains to be done in terms of trade in services, removing non-tariff barriers, and addressing other forms of regional integration necessary to the creation of a single market and production base (e.g., Tangkitvanich and Rattanakhamfu 2017). In the meantime, intra-regional trade has stayed remarkably constant in the range of about 25 percent of total trade over the past two decades (Figure 1), despite the dynamic trade sectors of its member-countries. Clearly, extra-regional markets, especially in Asia, continue to be critical to ASEAN.

Hence, the implications of the CPTPP, made up of eleven regional economies of which seven are ASEAN members, and RCEP, which includes all ten ASEAN countries as well as Australia, China, Japan, Korea and New Zealand (India dropped out of negotiations in 2019), are important to the direction of ASEAN economic cooperation in the future. The CPTPP went into effect in December 2018 and RCEP was signed in November 2020; both of these megaregional agreements have open accession clauses and membership will no doubt expand. While RCEP is less ambitious in terms of scope, it is a “living agreement” that will become more comprehensive over time.

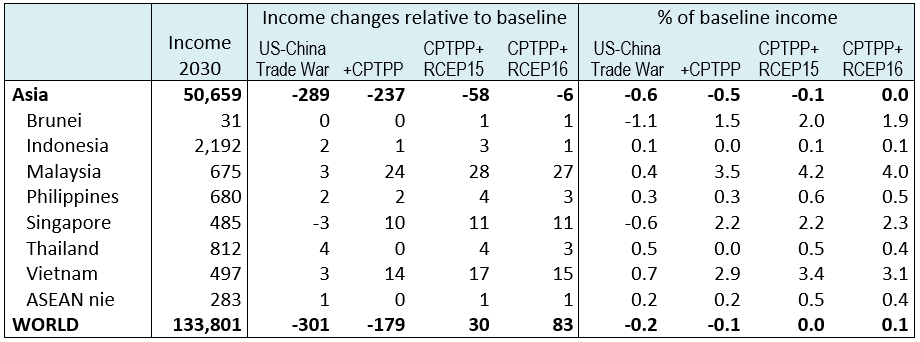

We apply a CGE model to estimate the direct effects of these megaregional agreements on ASEAN income in the context of the on-going US-China trade war (Petri and Plummer 2020). Results given in Table 1 capture changes relative to baseline income beginning in 2030. The US-China trade war is not expected to have a large aggregate effect on the ASEAN region; in fact, the only member-countries negatively affected are Singapore and Brunei. However, ASEAN members of the CPTPP benefit significantly from the agreement, especially Malaysia and Vietnam, and the effects on non-members are either marginal (Indonesia and Thailand) or even positive (the Philippines). Adding RCEP to the CPTPP enhances gains to the region. However, India’s joining RCEP (RCEP 16) actually has very little effect; indeed, a majority of ASEAN countries are (marginally) negatively affected by India’s membership.

Table 1

Real Income Effects of Trade War, CPTPP and RCEP on ASEAN, 2030

(US$ billion, equivalent variation)

Source: Petri and Plummer (2020)

Trade conflict, an impasse at the WTO, and the rise in Asia-Pacific megaregionalism combine to create myriad opportunities and challenges for ASEAN. By bringing down remaining barriers to ASEAN economic integration and harmonizing rules and disciplines, ASEAN would not only reap the benefits of deeper integration, which are substantial, but would also work more cohesively as a unit to help guide the direction of the CPTPP and RCEP, which in turn will have an important bearing on the future health and prosperity of the ASEAN economies. Given that ASEAN countries constitute a majority of both the CPTPP and RCEP memberships, the region would be in a good position to exert influence, provided it can leverage the community it has built up over the past five decades. When launched in 2012, RCEP was centered on “ASEAN centrality,” which can only be effective with a common, cohesive vision. Moreover, deeper integration will preclude any centrifugal forces that may tend to dilute ASEAN cooperation in non-economic areas, which are also critical to peace and prosperity in the region.

In sum, there is some urgency to implementing the AEC Blueprint 2025, which superseded the original AEC Blueprint 2015 launched in 2007. The formal entry into force of the AEC five years ago should be hailed as the beginning of a process of deepening integration, with the more difficult challenges still to be tackled from impediments to trade in services to the completion of the ASEAN Single Window in customs cooperation and beyond. The more integrated ASEAN becomes, the better position it will be in to thrive in the 21st century international marketplace. .

_________________________

Co-author Peter A. Petri is the Carl Shapiro Professor of International Finance in the International Business School at Brandeis University.

Co-author Fan Zhai is former Managing Director of the China Investment Corporation.

When you subscribe to the blog, we will send you an e-mail when there are new updates on the site so you wouldn't miss them.

Subscribe via ![]() in the tool bar.

in the tool bar.

Follow us on social media.

![]()

![]()

![]()