Co-authors: Wong Koi Nyen; Goh Soo Khoon

A large and young labor force has been instrumental in China's economic growth for several decades. The age structure of the population is shifting, however, with the population in the working age range of 15 to 64 declining steadily since 2015. A decades-long fertility rate of below replacement level and increasing life expectancy have produced a dramatic ageing of the population. Despite the government's introduction of pro-birth policies, the fertility rate remains low in 2023 at 1.7 per woman. The shrinking workforce is putting upward pressure on wages causing China to lose the low-cost advantage that has propelled its growth for so long. The rapid “graying” of the workforce over the next decade raises concerns about the future pace of economic growth. Such concerns were galvanized in 2022 when China's population declined year on year from 1.4126 billion to 1.4118 billion.

An aging population and low fertility could influence economic growth through a number of channels, notably labor supply, saving and investment, and the fiscal balance. Alongside the decline in the labor input to production, investment in physical capital could decelerate as the expanding share of elderly in the population brings down the saving rate. Further, the tax base will be diminished by the shrinking of the working-age population against a growing fiscal burden for healthcare and other support services for the elderlyplaces.

On the other hand, the urbanization that has been a major driver of China's growth over the last few decades, with hundreds of millions of people moving from agriculture to industry for great gains in productivity, still has room to run. The question is whether continued internal migration can compensate for the decline in the working-age population and whether as industrialization continues to move forward, more efficient firms can fill the labor supply gap through the utilization of labor-substituting technologies.

To determine the effects of demographic change and migration on economic output, we employed a quasi-structural model to estimate the relationships historically using data from 2001 to 2018, and then applied the estimated model to generate trajectories to 2060 (Goh et al. (2023).

The cointegration analysis of the historical data shows that there indeed exist long-run relationships between macroeconomic and demographic variables for each channel modeled, namely, labor force, saving, domestic investment, and fiscal balance. The estimated production function shows that both the urban working age population and the real capital stock have contributed significantly to real GDP. Further, the migration of workers from rural to urban areas has been a major source of total factor productivity growth.

|

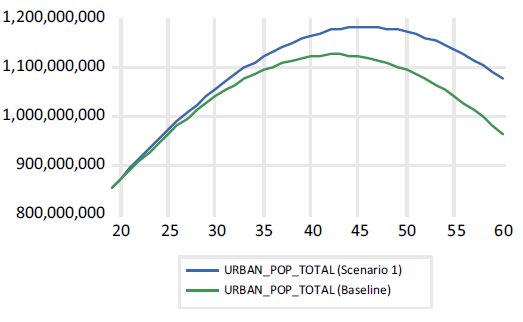

Figure 1. A. Urban population

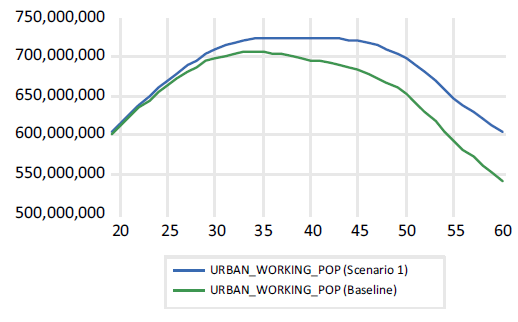

B. Urban working age population

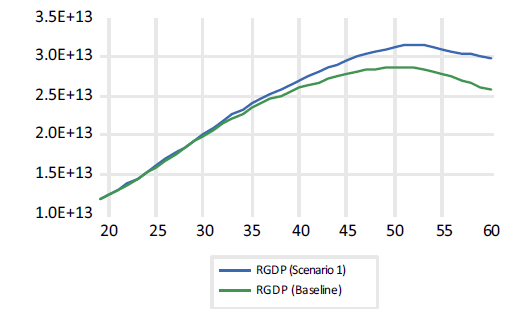

C. Real GDP

|

Model projections for urban population, urban working age population, and real GDP are shown in the three panels of Figure 1, respectively. Both a baseline scenario representing the mean stochastic forecast of the urban population and a high scenario representing the 95 percent confidence bound from that forecast are presented.

Under the baseline scenario, China’s urban population peaks in 2043 at 1,123 million people (Figure 1A). Under the high urbanization scenario, the peak is delayed until 2046 with the urban population reaching 1,180 million. The United Nations projection of China’s total population for 2045 is 1,429 million. Therefore, under the baseline projection the urbanization rate in 2045 is approximately 79 percent compared with 83 percent under the high urbanization scenario. The prospect for continued rise in the urban population over the next two decades suggests the ageing effect may not necessarily prevail to slow down economic growth.

However, even with growth in the urban population sustained until 2043 under the baseline scenario, the urban labor force peaks much earlier in 2034 at 705 million (Figure 1B). By the second half of the 2030s a declining urban labor force imposes a serious drag on the economy. Under the faster urbanization trajectory of the high scenario, the urban working age population roughly stabilizes between 2035 to 2045 providing somewhat more supportive conditions for economic growth. Within the total population, the working age share topped out already in 2010 at 73.8%, and under our projection this share continues to decline steadily to 56% in 2060.

The decline in the potential urban workforce imparts a drag on output growth. Meanwhile, the fiscal balance and the saving rate are projected to fluctuate over the forecast horizon as the share of elderly in the population peaks and then fluctuates. Throughout, growth in the capital stock remains strong enough to offset the negative demographic forces as far out as 2050 under the baseline scenario at which point real GDP reaches a peak (Figure 1C). Under the high urbanization scenario, growth remains positive for only a few years longer. Beyond mid-century, the shrinking working age population and declining rate of urbanization dominate to turn GDP growth negative.

The dire consequences yielded by the modeling exercise rest on a small number of factors. More broadly speaking, policy can play a role to alter the course of events. We highlight a couple of policy strategies. First, real investment has been a key source of China’s past economic growth, and will continue to be important through the projection horizon. Although some economists express concern over the diminishing marginal product of China's capital investment, future investment is likely to embody ever more advanced technology. The Chinese government has commited substantial resources to artificial intelligence, electric vehicles, green energy, semiconductors, and quantum computing, technologies that promise to drive productivity gains on through the 21st century. The analysis presented herein reinforces this strategy of investing in cutting edge technologies. Funding for these investments can be supported by high rates of public and private saving. Our projections of fundamental macroeconomic balances indicate that such funding is manageable under current and future demographic and economic trends. Second, policies governing rural-to-urban migration can be redesigned to better take advantage of gains to be had from shifting workers to higher productivity jobs in manufacturing, advanced technology, construction, and export sectors.

____________________________________

Co-author Wong Koi Nyen is Professor and Associate Dean (Education) at Sunway Business School, Sunway University, Selangor, Malaysia

Co-author Goh Soo Khoon is Associate Professor at the Centre for Policy Research & International Studies, Universiti Sains Malaysia, Malaysia