Co-Author: Roberto Meurer

The conclusion of the previous post in this series is that East Asia has worked out a policy routine for managing exchange rates in service to macroeconomic stabilization. For Latin America, by contrast, such a routine is not in evidence.

The essence of the East Asian model is for the central bank to counter macroeconomic shocks by leaning against exchange rate volatility. This means accumulating reserves when the local currency is strong and selling them off to mitigate depreciation. The bias must be toward accumulation as only by first accumulating reserves are central banks in a position to sell when the need arises. This tilts the exchange rate toward undervaluation of the local currency which carries the advantages of averting perceptions of overvaluation with their attendant potential to unleash capital outflows and of making local production more globally competitive.

|

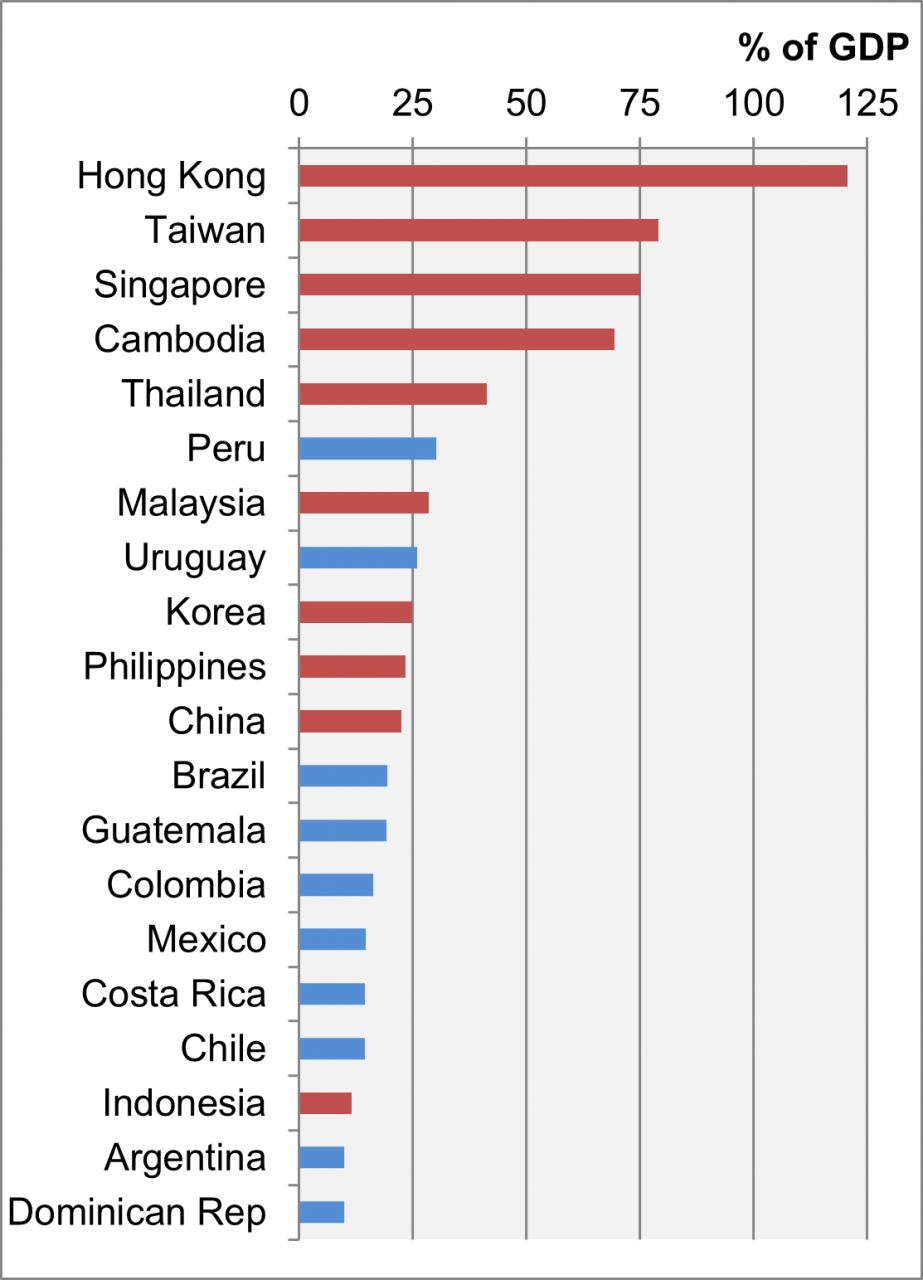

Chart 1: Official Reserves/GDP, 2019

Data Sources: IMF Balance of Payments and International Investment Position Statistics; Central Bank of Taiwan. (Vietnam data are not in the IMF database.) |

Chart 1 makes clear that the economies of East Asia have generally laid a stronger foundation for two-sided forex market intervention than those of Latin America. All but one economy in East Asia hold reserves in excess of 20 percent of GDP while all but two Latin American countries show ratios below this threshold. This leaves Latin American countries with more limited capacity to intervene against currency depreciation.

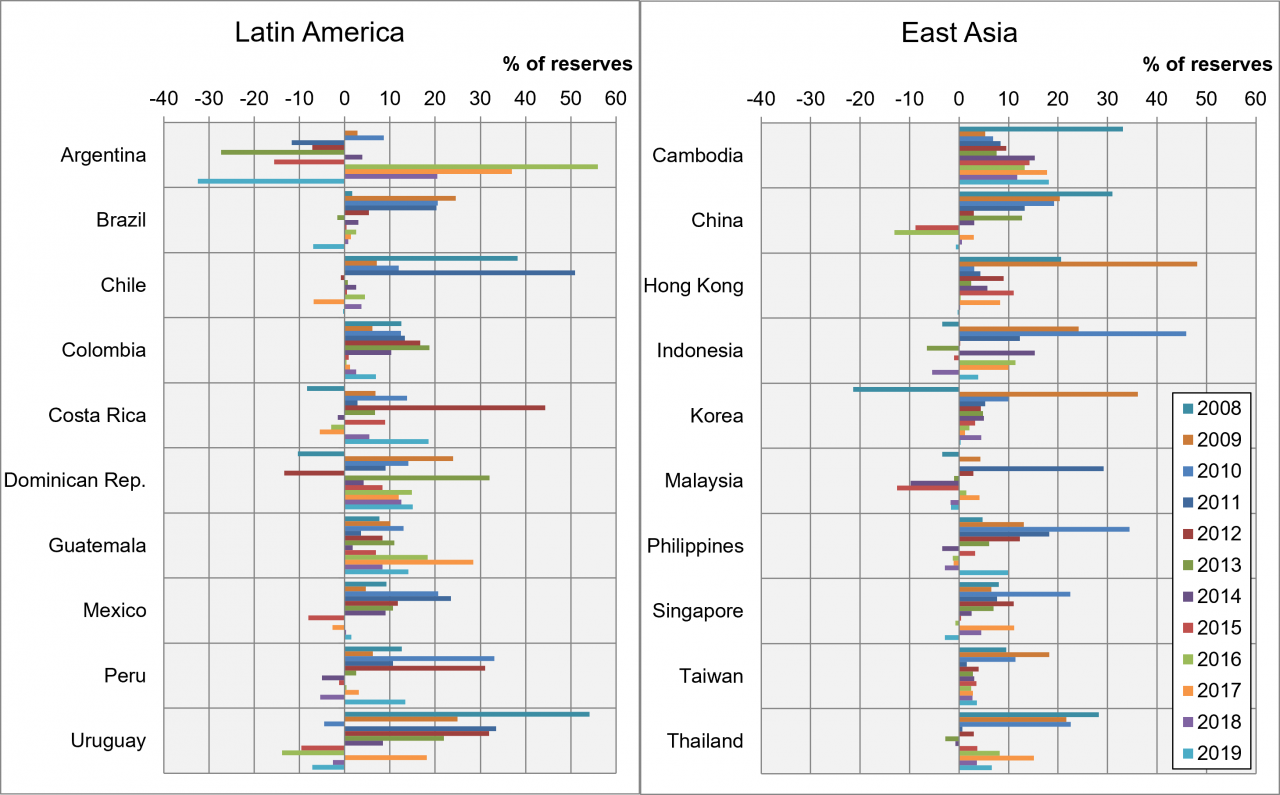

Chart 2 compares the records of intervention, captured by reserve flows as measured on the balance of payments relative to reserve stocks. Apart from Argentina, patterns are similar between the two regions although of note, for Latin America percentage changes in reserves are relative to smaller bases normalized on GDP. For both regions, the weight of intervention lies heavily on the side of reserve accumulation and magnitudes fluctuate greatly from year to year.

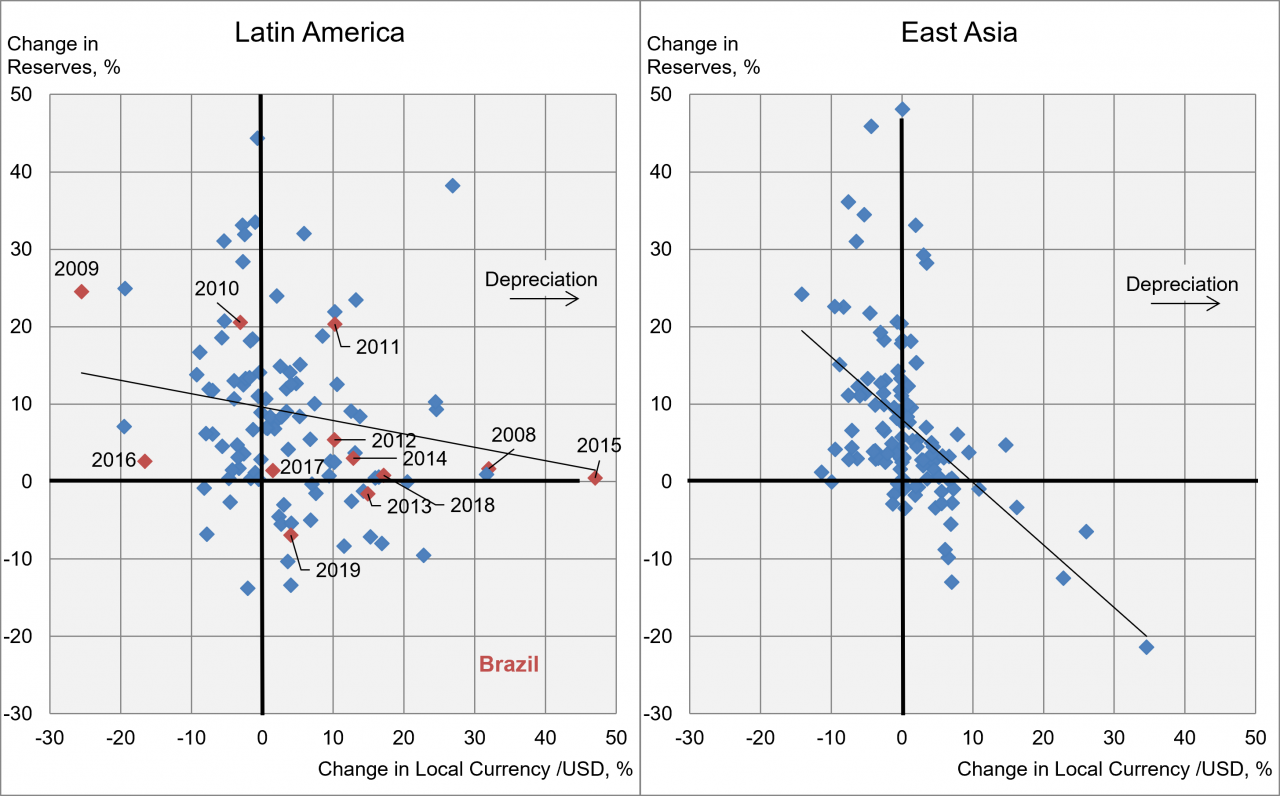

Turning to Chart 3, the difference in policy behavior between the two regions becomes manifest. Whereas in East Asia reserve accumulation varies systematically with exchange rate movement, in Latin America the association is more random. In the outer reaches of the upper right quadrant, Latin American central banks are seen to accumulate reserves (sell domestic currency) even as the domestic currency is depreciating. Conversely, in the lower left quadrant, they decumulate reserves (buy domestic currency) even as the domestic currency is appreciating. Thus, they sometimes lean into exchange rate movement rather than consistently leaning against it as in East Asia.

|

Chart 2: Change in Reserves, 2008-2019

Chart 3: Change in Reserves vs Change in Exchange Rate, 2008-2019

Note: Change in reserves is measured as balance of payments flows relative to reserve stocks. Argentina is excluded from Chart 3. Data sources: IMF Balance of Payments and International Investment Position Statistics; IMF International Financial Statistcs; Central Bank of Taiwan. |

The exchange rate referenced is the nominal rate with respect to the US dollar. If inflation were higher and more variable in Latin America than in East Asia, that would loosen the relationship between the nominal exchange rate and reserves since inflationary episodes would call for nominal depreciation to preserve real exchange rate parity without need of central bank action. Excepting Argentina, however, inflation has been moderate in both regions, East Asia showing an average rate of 2.6 percent with standard deviation of 2.5 and Latin America an average of 5.0 percent with standard deviation of 2.5. Whether the charts are constructed on the basis of real or nominal exchange rates, then, does not alter the conclusion of contrasting policy approaches.

The greater dispersion of points in the horizontal dimension for Latin America implies more exchange rate volatility has been tolerated without central bank intervention to counter it. Mean rates of change in exchange rates differed little between the two regions, Latin American registering depreciation at 3.9 percent a year versus 0.8 percent for East Asia, a differential roughly in line with the gap in inflation rates. Yet the standard deviation for Latin America was 10.8 versus just 6.7 for East Asia. One might imagine that this would correspond to less variability in reserve accumulation for Latin America but in fact the opposite is the case. Average rates of reserve accumulation were similar between the regions at 8.9 percent for Latin America versus 7.3 percent for East Asia even as standard deviations again diverged notably – 12.7 Latin America versus 10.9 for East Asia. This means Latin American central banks have intervened more unevenly and yet without directing this intervention toward exchange rate stabilization.

Brazil is behind a number of the outliers in Chart 3. The country was whipsawed by the Great Financial Crisis as initially capital outflows to the US safe haven caused the Brazilian real to depreciate by 32 percent in 2008, following which expansionary US monetary policy flooded emerging markets with capital seeking yield. In 2009, the real was held to a regaining of its losses under strong intervention by the central bank that increased reserves by 25 percent. Through 2010 and 2011, the central bank continued its purchases, to the point of engineering a 10 percent depreciation of the real in 2011 in an effort to push back against the real’s elevated level relative to historic valuations. In the course of three years of aggressive forex buying, reserves rose from $194 billion in 2008 to $352 billion in 2011.

The next few years saw continued depreciation in the real with modest reserve accumulation by the central bank. The government favored currency depreciation as a way to stimulate domestic output. More vigorous stimulus extended to tax cuts and expansion of subsidized credit by state banks. Not surprisingly, fiscal deficits mounted and inflation picked up, consumer prices rising by more than 10 percent in 2015. Growing economic uncertainty undermined support for President Dilma Rousseff, with this culminating in her her eventual ouster. The political tumult sent the real into a tailspin, its value plummeting by 47 percent in 2015. With accession of Michel Temer to the presidency, confidence was restored and the real rebounded in 2016. The central bank remained on the sidelines throughout this episode leaving the exchange rate to absorb the full brunt of the shock.

In October 2018, Jair Bolsonaro was elected president on a pro-market platform that included promises to control fiscal deficits and privatize state enterprises. The new administration took office on 1 January 2019 on the heels of depreciation in the real that reached 17 percent in 2018. The central bank showed willingness to intervene against continued depreciation in 2019, releasing 7 percent of its reserves to hold the rate of depreciation to 4 percent. Perhaps this is a sign of a more engaged stance to come.

East Asia has crafted an effective approach to moderating the volatility of market-oriented exchange rates. Compared to Latin America, both exchange rates and reserve holdings have been more stable in the region, as shown in Chart 3. Whether the East Asian model can be adapted to the Latin American context is an open question.

_______________________

Co-author Roberto Meurer is a professor in the Department of Economics and International Relations at Federal University of Santa Catarina, Brazil.

When you subscribe to the blog, we will send you an e-mail when there are new updates on the site so you wouldn't miss them.

Subscribe via ![]() in the tool bar.

in the tool bar.

Follow us on social media.

![]()

![]()

![]()