This post follows up on my review of Tom Orlik's wonderful book "China: The Bubble that Never Pops". The book explains why constant predictions of China's economic collapse due to mounting debt and financial risk have not been borne out, and the explanation is altogether compelling. My one quibble with the book regards Orlik's view of the underlying driver of the saving/consumption imbalances that motivated debt driven stimulus. Orlik emphasizes China's one-child policy as the source of the imbalances, going so far as to call it China's original sin in an interview. The argument is that with China's weak social welfare system, having only one child makes for insecurity about old age that induces parents to save more during their working years. I'm not convinced that this holds up as a reason for China's imbalances. Let me hasten to add that, regardless, the book's original contribution in explaining why no crash has occurred holds up very well. The source of the imbalances is a separate issue, but one worth pursuing in its own right.

There is a sense in which I agree that the one-child policy has been a factor in China's high saving. The exceptionally sharp decline in the birth rate in China's case accentuated the demographic transition that is common among countries during economic development. A couple of decades on, the drop in the birth rate brings a bulging labor force relative to a shrinking share of old and young age dependents in the population. Per the life cycle hypothesis of Modigliani (1970), saving is done by those in their working years who generate income whereas the young and old consume without producing any income from which to save. The decline in China's dependent share was particularly steep in the 2000-aughts and relatedly, so was the rise in the saving rate, as shown by Bonham and Wiemer (2013). So while the one-child policy mattered, it did not matter until two decades after it was introduced and not because it prompted precautionary saving to provide security in old age but because of the long-run demographic forces it intensified.

Besides demographics, Bonham and Wiemer argue that GDP growth is an important determinant of movement in the saving rate. Theories of the relationship between income growth and saving are well established in the literature (Friedman, 1957, on the permanent income hypothesis; Carroll, Overland, and Weil, 2000, on habit formation). Empirically, the Chinese experience bears out the relationship, as do the experiences of other East Asian miracle countries.

Teasing out the relationship in the Chinese case requires some manipulation of the official GDP data. In general, I don't subscribe to the view that China's GDP accounts are faked. The GDP accounts involve a massive complex of numbers that must line up internally in all sorts of ways, including over time, such that faking would be exceedingly difficult. However, there is one final step in getting to the headline GDP growth rate that is easy to fudge. That final step involves deflating nominal growth to obtain growth in real terms. Bonham and Wiemer undertook the exercise of computing a GDP deflator based on sectoral inflation rates to derive a real GDP growth series that shows much sharper fluctuations than the official series. A bit of fudging in the official figures appears to have moderated the extremes, both low and high.

The derived GDP growth series fits well with standard theory that predicts high GDP growth will result in a rising saving rate and low GDP growth in a falling saving rate. The figure below plots China's saving rate from 1979 to 2018 distinguishing four periods in different shades of red. We focus analysis on periods 2-4 and lump diverse sub-periods together in period 1. Overall, growth in period 1 averaged a decent 8.9% a year with the saving rate ending at 41.8% in 1994, about 5 percentage points higher than when the period began in 1979.

|

Saving Run-Ups and Average GDP Growth Rates Data sources: GDP growth rates for China, 1979-2008, Bonham & Wiemer (2013) calculations; Taiwan data, Republic of China Statistical Bureau; all else, World Bank World Development Indicators. |

Period 2 runs from 1994 to 2000, during which time the saving rate declined to 36.4%. This period saw China's version of big bang reform. The state sector was significantly downsized, housing was privatized, and many people lost their jobs. All this was highly disruptive but prepared the way for more efficient development going forward. The derived GDP growth rate for this period was by Chinese standards a rather dismal 5.9% a year. Under such diminished growth, consumption rose faster than income and the saving rate fell.

The reforms of the late 1990s in combination with China's entry into the World Trade Organization in 2001 powered a long economic boom. The derived growth rate for period 3 registers at 12.0% a year. Accordingly, the saving rate was pushed ever higher to hit 50% in 2008.

Period 4 saw slower growth, with the official figure given at 7.5% a year, and the saving rate headed back down.

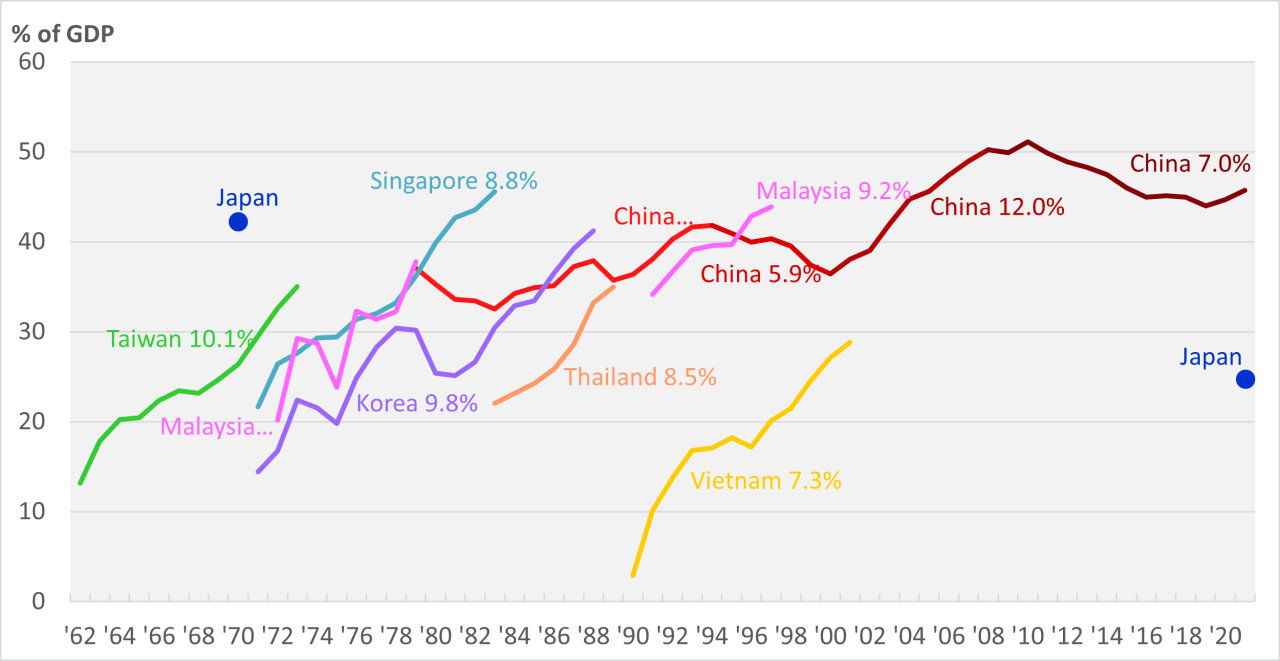

China's run-up in saving during the hyper growth of the 2000-aughts echoes the earlier experiences of East Asian countries during their development take-offs. Taiwan achieved average growth of 10.1% a year from 1962 to 1973, with its saving rate rising from 13.2% to 35.0%. Singapore came next with growth of 8.8% from 1971 to 1983 and a saving rate increase from 21.7% to 45.6%, and Korea followed with growth of 9.8% from 1971 to 1988 and a saving rate increase from 14.4% to 41.2%. Malaysia went through split episodes of rapid growth coupled with saving increases in the 1970s and 1990s; Thailand had a spurt in the 1980s; and finally Vietnam followed along in the 1990s.

Eventually, growth must slow and the demographic transition runs its course to deliver an ageing population. With this, the saving rate tracks back downward. Japan has led the way with its saving rate declining from 42.2% in 1970 to 24.6% in 2018. This augers China's future.

What is exceptional about China is that its saving rate started at a level that was already high at the beginning of the reform era, and with ups and downs in between was that high again at the beginning of the 2000s when growth exploded. As the saving rate rose ever higher, investment and/or net exports had to replace consumption as demand drivers. Good investment opportunities are hard to come by at a level of more than 40% of GDP, and expanding net exports proved unpopular with the rest of the world. Picking up the story here, Orlik tells of debt fueled investment to sustain growth and what was then done to keep the bubble from popping, all very informatively.

The backstory behind the imbalances, I would argue, rests first and foremost on China's very success in achieving extraordinarily rapid growth. The one-child policy and the weak social welfare system had little if anything to do with it. Growth at the pace China experienced in the 2000-aughts is inherently unbalancing. Consumption does not keep pace with output growth, and demand must therefore be sustained by investment or net exports. China is no different from any other country in this regard except, of course, in its globally more consequential scale.

When you subscribe to the blog, we will send you an e-mail when there are new updates on the site so you wouldn't miss them.

Subscribe via ![]() in the tool bar.

in the tool bar.

Follow us on social media.

![]()

![]()