US interest rate hikes in 2022 have drawn global capital away from the rest of the world to put downward pressure on currency values vis a vis the dollar. To defend their exchange rates, many Asian central banks have sold off reserves. A future post will provide an overview of the situation as data become more broadly available. For Taiwan, data already in hand reveal a surge in capital outflows. For the first half of 2022, net portfolio outflows reached $77 billion versus average full-year magnitudes hovering around $60-80 billion for most of the past decade. Even in the context of a rush of global capital out of emerging markets, the Taiwan case is extreme. Nevertheless, a modest accumulation of official reserves has continued to prevail on the balance of payments.

|

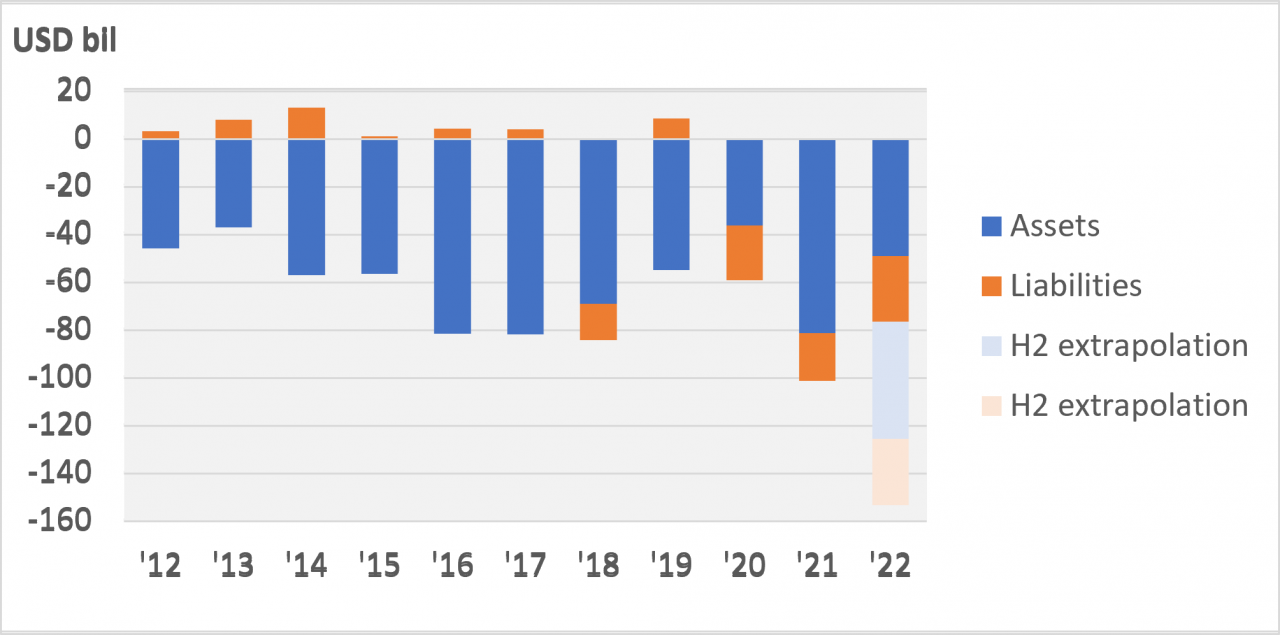

Chart 1: Portfolio Asset (Outbound) and Liability (Inbound) Flows

Data source: Taiwan Central Bank |

Chart 1 shows asset (outbound) and liability (inbound) flows for portfolio investment. Net asset flows consistently register as negative meaning Taiwan residents have been acquiring foreign assets to a greater degree than than they have been liquidating them. Net liability flows, which are much smaller in absolute value, have turned negative in recent years meaning foreign residents have been liquidating investment in Taiwan to a greater extent than they have been injecting new investment. This may suggest growing concern about Taiwan's security, and perhaps, too, unease about its reliance on semiconductors as a mainstay in the face of US efforts to bring production home.

The surge in portfolio investment outflows must be offset elsewhere in the balance of payments. Taiwan has long maintained substantial current account surpluses. The magnitudes increased with the pandemic from around $70 billion a year in the late 2010s to $95 billion in 2020, $114 billion in 2021, and for the first half of 2022, $57 billion, which is on par to match 2021. So, although current account surpluses have historically been in rough alignment with portfolio capital outflows, there was no sharp increase in the the current account surplus in 2022 H1 to match the increase in portfolio outflows.

|

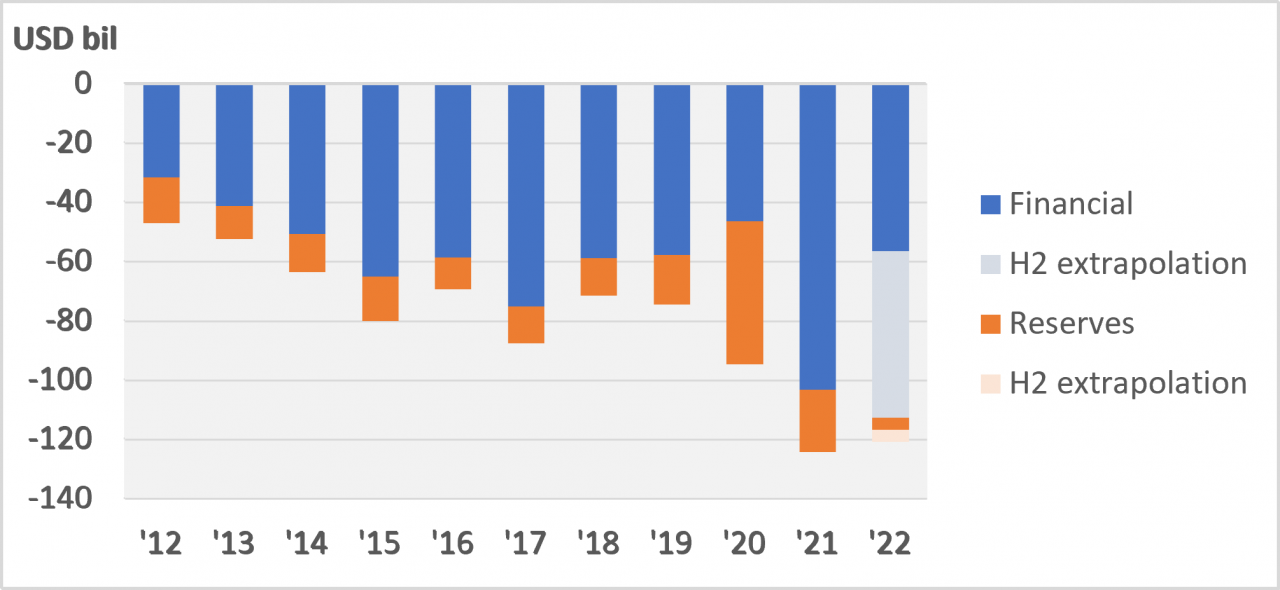

Chart 2: Balances on Reserve & the Financial Account

Data source: Taiwan Central Bank |

For many Asian economies, the central bank has stepped in to play the balancing role by selling reserves (a balance of payments credit) against capital outflows (a debit). That was not the case for Taiwan, however. Chart 2 shows that reserve accumulation continued in 2022 H1, albeit at the slowest pace in a decade. Also clear from Chart 2 is that overall financial outflows did not take nearly the leap that portfolio flows did in 2022. That means the main offset to increased portfolio outflows must lie somewhere within the financial account.

The shift in the balance on "other investment" is a large part of the story, the net credit position rising from under $4 billion in 2021 to about $24 billion in the first half of 2022 for an annualized increase of $44 billion vs the annualized increase in debits for portfolio flows of $52 billion. Other investment captures a variety of items and tends to be highly volatile even under normal circumstances, so locating the offset here does not shed much light on the balancing mechanism involved.

It is worth noting in this connection, however, that the central bank of Taiwan (CBC) works in mysterious ways according to Brad Setzer and a co-author who goes by S.T.W. writing in 2019 for the US Council on Foreign Relations. Considerable detective work led these authors to conclude that the CBC had hidden a cumulative $130 billion in reserves (20 percent of Taiwan's GDP) off its balance sheet in FX swaps. The transactions would presumably have been recorded on the balance of payments under other investment (IMF Balance of Payments Manual, p. 137).*

The backdrop for the inquiry was Taiwan's sustained large current account surpluses against relatively modest annual increments to official reserves. The explanation Setzer and S.T.W. arrived at for this schism is that behind the scene the CBC, acting through commercial banks, has been providing a hedge for life insurance companies that invest in foreign bonds. Life insurance companies are a major savings vehicle for Tawainese households. Insurers can get a better return on their holdings by investing overseas, but this leaves them with a mismatch on their balance sheets between USD assets and TWD liabilities. To hedge this exposure, they enter into FX swaps, pairing an exchange of TWD for USD now with a forward contract to exchange USD for TWD at a predetermined rate in the future. The CBC has the ample USD needed to act as the counterparty in such swaps, having borne heavy purchases of USD to keep the TWD from appreciating under the pressure of ongoing current account surpluses. To wrap this up neatly, the CBC, when it makes the spot exchange of USD for TWD, simply eliminates the TWD, effectively sterilizing its prior forex market intervention. When the swap contracts come due, they are rolled over, perpetually, keeping the insurance companies ever hedged.

Setzer and S.T.W. argue that there are drawbacks to this arrangement. For one, the CBC's stabilization of the exchange rate leaves many agents not bothering to hedge their USD exposures, including insurers for a substantial part of their portfolios. More systemically treacherous, the CBC "has dug itself into a financial hole ... by investing too much of its national savings abroad – and thus leaving its population exposed to financial losses when its currency inevitably appreciates." But most vexingly for Setzer and S.T.W., Taiwan has gotten away with concealing behavior that every other major economy in the world must report under IMF mandate because it is not an IMF member. And this allows it to fly under the radar on the kind of "currency manipulation" that Setzer has doggedly fought against.

So, what did Taiwan's central bank do in 2022 in response to the global shock to portfolio capital flows? It is not transparent, if Setzer and S.T.W. are to be believed. But the large surpluses under other investment could be the trace of it backing away from rolling over FX swaps.

__________________.

*This assumes the currencies underlying the FX swap were delivered, rather than cash settlement taking place on the basis of the value of the derivative contract at maturity, which method would have failed to remove reserves from the CBC balance sheet.

When you subscribe to the blog, we will send you an e-mail when there are new updates on the site so you wouldn't miss them.

Subscribe via ![]() in the tool bar.

in the tool bar.

Follow us on social media.

![]()

![]()

![]()