In May 2013, Ben Bernanke, Chairman of the US Federal Reserve Bank, hinted at the possibility of the Fed reducing (“tapering”) its purchases of government bonds sooner than previously expected, leading to a reassessment of the likely path of US monetary tightening. Market turbulence and economic volatility in emerging market countries (EMs), including those in Asia, quickly followed. Capital inflows turned to outflows, leading interest rates to rise, asset prices to decline and—despite a run-down of foreign reserves—exchange rates to depreciate. This event came to be known as the Taper Tantrum.

|

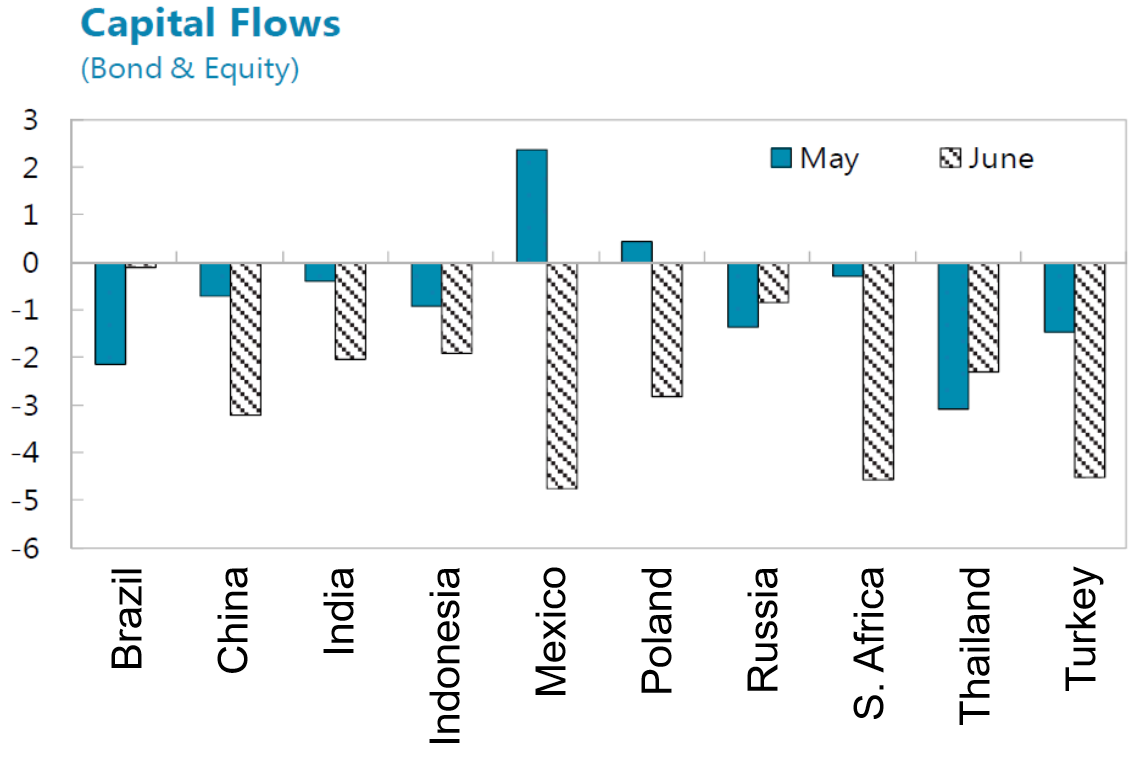

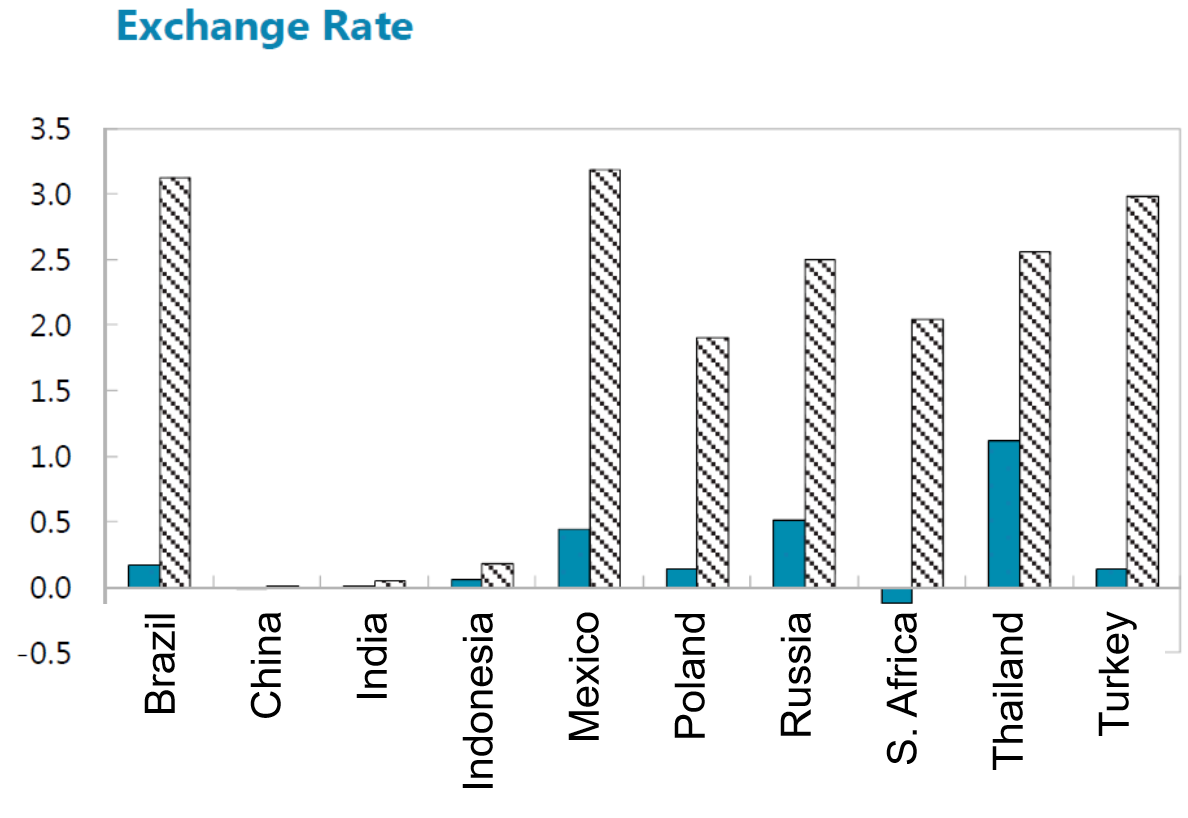

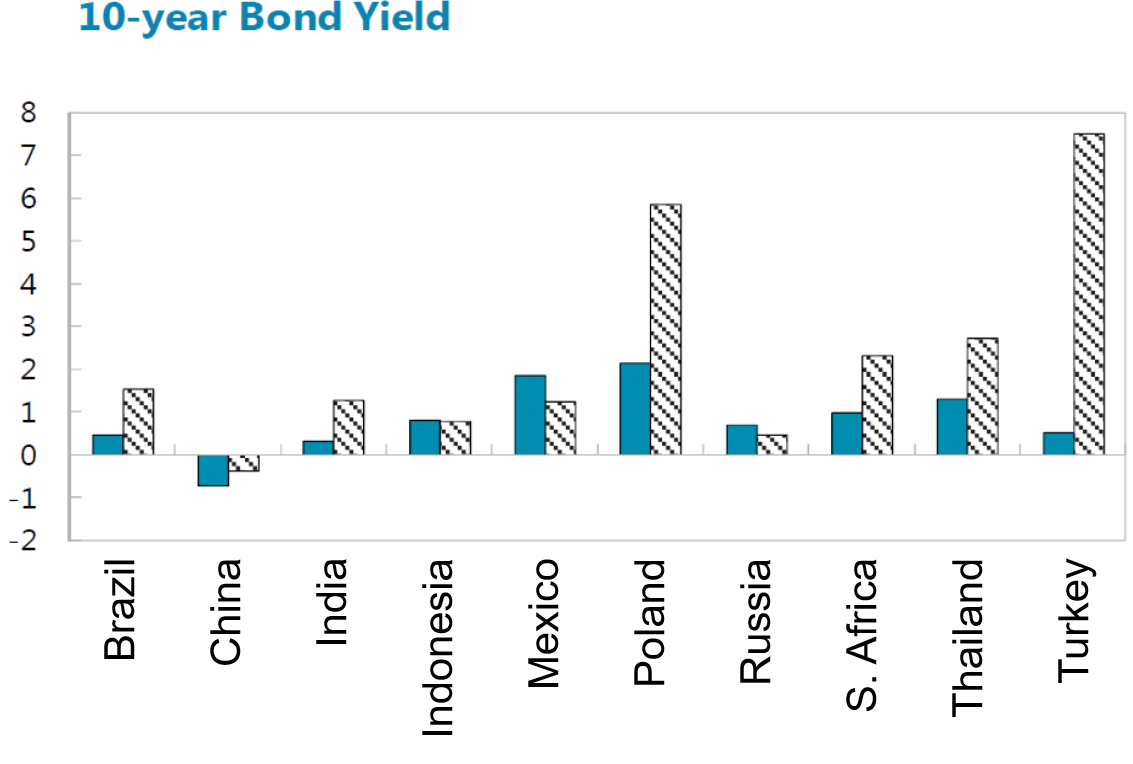

Figure 1: Effect of 2013 US Monetary Policy Shock on Emerging Economies

Source: IMF, Emerging Market Volatility: Lessons from the Taper Tantrum, 2014, Figure 16. |

While the direction of these changes should have been no surprise, their size and speed were, reflecting the very accommodative global financial conditions at that time, as well as the surprise nature of Bernanke’s comments. Figure 1 shows the large but differentiated impact on key financial variables (normalized by historical variances, yielding so-called z-scores) over the initial months of the taper tantrum. Those countries most affected by the taper tantrum tended to be characterized by large current account deficits financed by easily-reversed portfolio flows, large forex-denominated debt. sizable fiscal deficits, and weak growth. Among Asian countries, Indonesia, India, and Thailand all took significant hits.

One does not need to look too hard to see similarities to today. As in 2013, global financial conditions are highly accommodative, with interest rates at or near historical lows. EMs, after an initial loss of capital in the early days of the pandemic, have found themselves on the receiving end of sizable capital flows. And pandemic-related spending has pushed up deficits and debt levels throughout the global economy. Moreover, as in 2013, the Fed may soon face difficult monetary policy choices that have the potential, once again, to surprise global markets.

Most analysts are expecting a sharp recovery in the US—supported by the rollout of vaccines, massive fiscal stimulus, and a large pool of household savings. The Fed, in particular, recently upgraded its projections of growth and inflation for 2021, to 6.5 and 2.2 percent, the latter above its target of 2 percent. Despite this much-improved outlook, the Fed has downplayed inflation concerns and highlighted its intention to continue its current monetary stance until the US achieves full employment and actual inflation at or above its target for some time. In fact, the median expectation among Fed board member is that the next rate hike will take place only in 2024.

But there are significant uncertainties about how the recovery will play out, and upside risks to both growth and inflation. Last week’s very strong US jobs report underlined the very real possibility that the recovery may be quicker, and inflation higher, than currently expected, leading the Fed to tighten policy earlier and more than planned. Absent clear communication from the Fed and appropriate policy responses from EMs, we may well see the sort of shock to the Asia region that we saw eight years ago.

It should be noted that an orderly rise in US interest rates, particularly if reflecting higher growth, need not have a negative impact on Asian EMs. Indeed research suggests that the positive impact on capital flows to EMs of higher US growth can more than offset the negative impact of higher US rates (IMF, 2014). Also, Asian EMs are well-placed to deal with market volatility. For instance, Indonesia, Thailand, and India, have seen current account deficits reduced or converted to surpluses since 2013, and foreign reserves remain large.

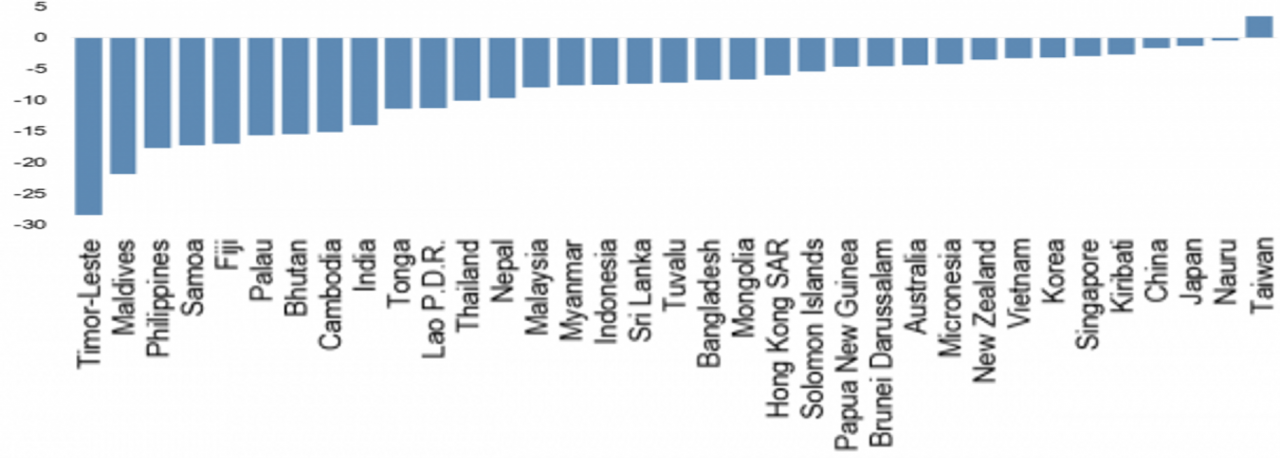

On the other hand, should US rate hikes again surprise, or should they reflect higher inflation rather than growth, capital outflows from Asia would be more likely. Moreover, Asia is—like the rest of the world—still recovering from an enormous economic shock (see Figure 2.) Thus, a new taper tantrum now could stall a long-awaited recovery.

|

Figure 2: Output Losses Due to Covid

Note: Output losses are calculated as the difference in cumulative growth rates (2020-22) between current versus pre-Covid projections. Source: IMF Blog, 2021. |

A new taper tantrum would also confront Asian central banks with difficult choices. With economies still on the mend, they would need to decide between matching US rate hikes to protect against outflows and depreciation, and maintaining or lowering rates to support growth, while perhaps intervening in the foreign exchange market to support the domestic currency. In recent weeks, several large EM central banks made monetary policy decisions in the context of already-rising US rates: Brazil, Russia, and Turkey all raised rates, while South Africa kept theirs unchanged.

When you subscribe to the blog, we will send you an e-mail when there are new updates on the site so you wouldn't miss them.

Subscribe via ![]() in the tool bar.

in the tool bar.

Follow us on social media.

![]()

![]()

![]()