As we stumble out of the global COVID-19 pandemic, we need to examine how our economies have changed. In East Asia, the pandemic may result in higher costs for travel. In addition, the well-publicized disruptions to supply chains may not prove transitory. As a result, the East Asian development model of manufacturing goods for export may be less reliable.

This suggests a need to review contemporary economic policy. This piece looks at the shortcomings of exchange rate policy in Southeast Asia. A longer paper is available that provides full references to the relevant literature.

Lack of an ASEAN Exchange Rate Policy

The Association of Southeast Asian Nations (ASEAN) is an important forum for encouraging economic development. The commitment to create the ASEAN Economic Community (AEC) in 2015 was a singular expression of the importance of regional cooperation. The AEC “envisions ASEAN as a single market and production base, a highly competitive region, with equitable economic development, and fully integrated into the global economy.” (Invest in ASEAN)

These goals are challenging, comparable to those that guided the creation of the European Union (EU), which purposely focused on being a common market with a common currency. In Europe, it was understood that this would require convergence of economic policy and outcomes. This was spelled out in the Maastricht Treaty, which emphasized the need to have relative stability of exchange rates.

I look at regional exchange rate configurations using Cronbach’s alpha (α), a measure used to check the internal consistency of education or psychology tests. It is designed to measure the “extent to which all the items in a test measure the same concept….” (Tavakol and Dennick, 2011) In this paper, the concept is a hypothetical regional currency, and the items are the individual countries. I look to see if regional exchange rates move in a common fashion.

In Equation 1, c is the average value of the covariance coefficients between the exchange rates of the k different countries, and v is the average of the country variances. I look at the U.S. dollar exchange rate because it is typically the headline exchange rate, affecting household and business plans. There is no standard scale for foreign exchange rates, so the series were normalized to have mean zero and standard deviation of 1. Thus v is a constant, and α is a nonlinear function of c, the average covariance, or equivalently the correlation coefficient. By construction, α is bounded from above by one and increases with larger k. Typically, values above 0.9 are considered to show a consistent test. (Green, 1995)

| Eq. 1 |

|

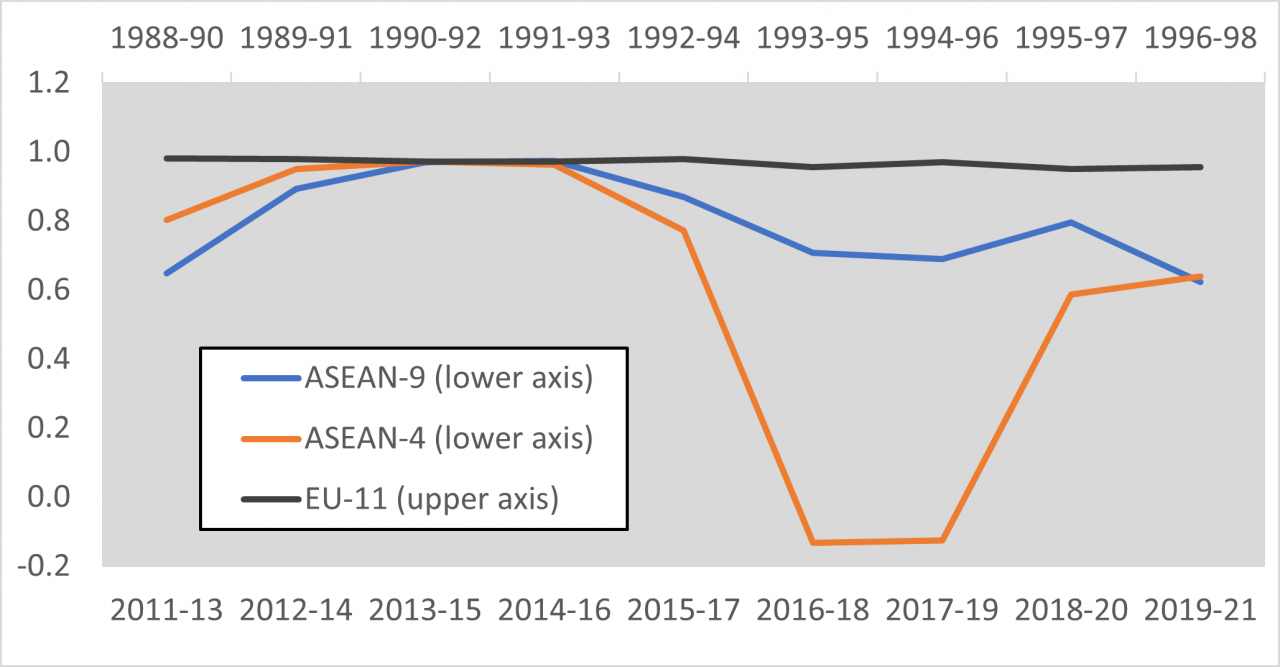

Figure 1: Cronbach's Alpha for USD Exchange Rates, ASEAN vs EU |

Figure 1 shows the values of α for different country groups. For Europe, I look at the eleven signatories of the Maastricht Treaty with independent exchange rate policies over the decade before the introduction of the euro in January 1999, forming rolling three-year values of α.

The European example shows how policy commitments can bring about similar economic outcomes: Cronbach’s α suggests that the individual exchange rates moved in similar fashion, collectively foreshadowing the expected regional currency.

Of course, one number can only convey so much concerning the dynamics of the movements of 11 exchange rates. The stability of the Euro-11 α masks offsetting changes in bilateral correlation between (i) the United Kingdom’s currency and the other European currencies, which turned negative over the period, and (ii) that of Greece, which saw a substantial increase in correlation with its partners. In the end, the U.K. did not join the common currency union; Greece did.

The current situation in Southeast Asia is quite different from pre-common currency Europe. ASEAN members have different institutional arrangements for managing foreign currency exchange rates. (IMF, 2020; Kawai, 2010) Some employ floating exchange rates (Indonesia, Malaysia, Philippines, and Thailand) others a crawl-like arrangement where changes are damped (Cambodia, Lao PDR, and Singapore).

Although there is no centrally directed exchange rate policy, stable interrelationships could occur due to regional capital flows or similar central bank goals and strategies. (Wiemer, 2021) ASEAN currencies are also susceptible to common shocks, such as during the Asian Financial Crisis in 1997.

However, similar concerns and susceptibility to shocks do not guarantee parallel foreign exchange movements. Figure 1, for instance, shows that in ASEAN, the value of α dipped noticeably in 2017-2019, with the average bilateral correlation coefficient falling from 0.81 in 2014-2016 to 0.20 in 2017-2019. In some instances, this appears to reflect different points in the domestic business cycles across the region. For example, in 2018, Thailand’s central bank raised domestic interest rates while Indonesia noticeably paused rate increases. (Bloomberg, 2018)

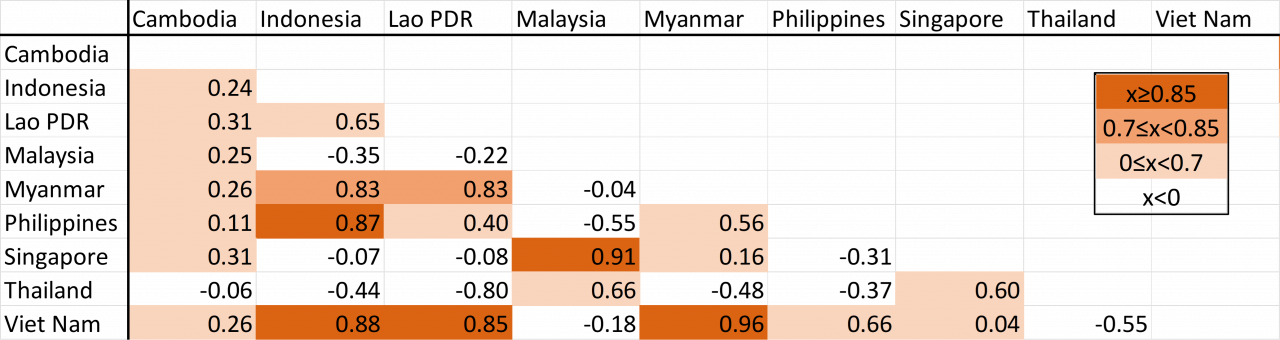

Table 1 illustrates the diversity of outcomes, showing the bilateral correlation coefficients between the various ASEAN currencies from 2017 through 2019. There is little joint movement, with 14 of the 36 bilateral correlation coefficients being negative.

|

Table 1: Bilateral Correlation Coefficients for USD Exchange Rates, 2017-19

Cronbach's α = 0.69. Average bilateral coefficient = 0.20. |

Implications of Disparate Exchange Rates

Are there costs to uncoordinated exchange rate policies in ASEAN? There has been no commitment to fashion a Southeast Asian equivalent to the euro. There have been intergovernmental discussions on the subject. There is also considerable academic literature. (Capannelli and Gochoco-Bautista, 2009; Kusuma et al., 2013; Ogawa and Shimizu, 2011; McAleer and Nam, 2005; and Green, 1995.) Forging a regional currency would incur both costs and benefits. For the former, countries would have to forgo independent monetary policy. For the latter, reducing uncertainty about relative exchange rates might encourage intra-ASEAN, cross-border investment, which has stagnated over the last decade. It might also quicken the convergence of living standards, lifting per capita income in the poorer nations.

Conclusion

As new challenges emerge for ASEAN, the lack of a coordinated exchange rate policy increases the uncertainty of business decisions. Although ASEAN has never moved to adopt a regional currency, increasingly there is a need to reconsider the issue. In this discussion, Cronbach’s alpha provides a useful measure of exchange rate dynamics.

When you subscribe to the blog, we will send you an e-mail when there are new updates on the site so you wouldn't miss them.

Subscribe via ![]() in the tool bar.

in the tool bar.

Follow us on social media.

![]()

![]()