The promise of development economics is that living standards can be raised significantly and sustainably. More than any other region, East Asia offered the hope that with the right policies, a country could reduce the incidence of severe poverty and, in some cases, provide for affluent lifestyles. Following Japan, buoyed by exports to the West, economies such as South Korea and Singapore grew their manufacturing sectors, transferring workers from low-productivity agricultural employment and raising overall living standards to that of the wealthier Western countries. Today, China continues this process, with the incidence of severe poverty falling from more than 66% of the population in 1990 to less than 1% in 2020 as it became the world's manufacturing center (World Bank).

The question for this note is whether the countries on the left-hand side of Table 1 are following the path of the Asian high-flying economies on the right-hand side. Can the poorer countries of Southeast Asia move up to the standard of living found in the group of more affluent countries? Can incomes converge at a high level across Southeast Asia? Some countries, including Malaysia and Thailand, have made this a national planning goal.

|

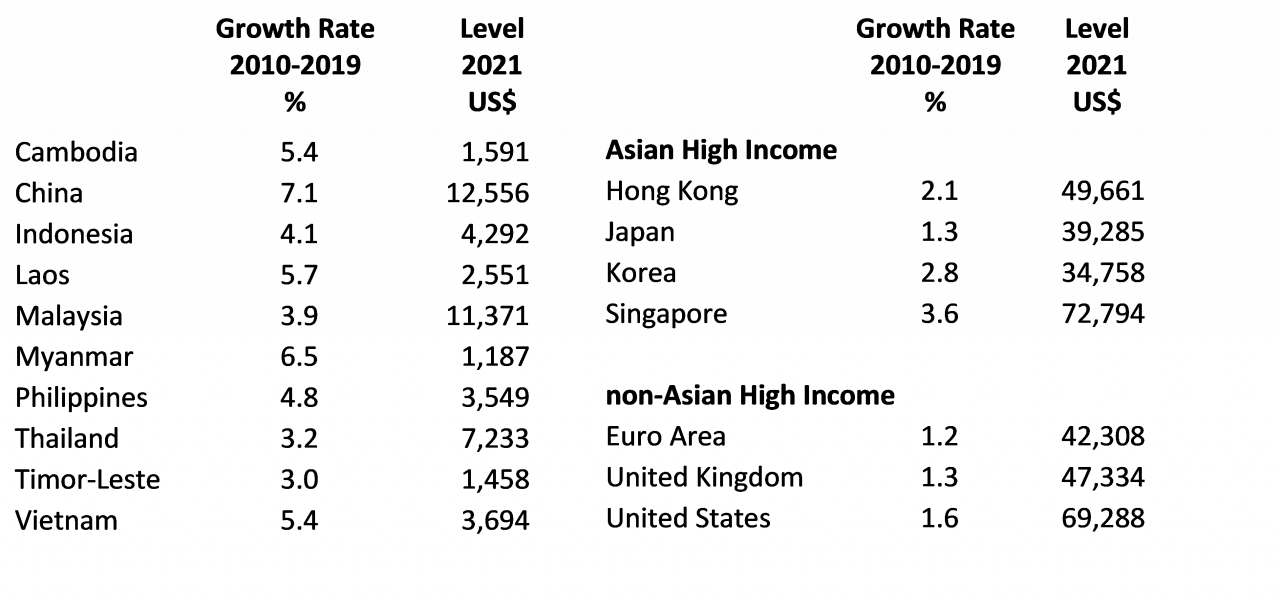

Table 1: GDP per capita real growth rate and level for East Asia and comparator economies

|

Much depends on the assumed relative growth rates. Looking at the immediate past gives a sense of what might be achieved. As reference, Table 1 shows average annual growth in real GDP per capita for 2010 to 2019, avoiding both the Global Financial Crisis and the Covid-19 pandemic.

|

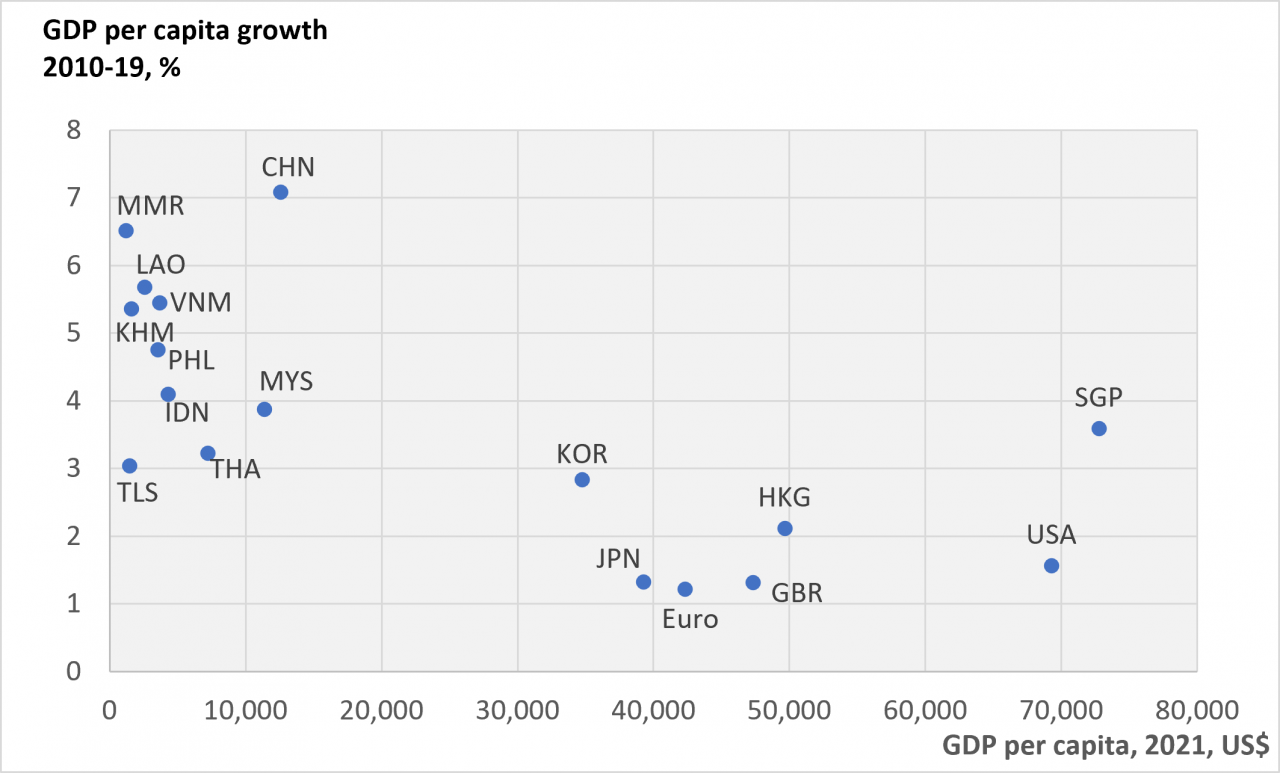

Figure 1: GDP per capita real growth rate vs level

Data source: World Bank, World Development Indicators. |

At first glance, there seems to be reason to hope for high-level convergence, as the poorer countries generally have grown faster than the more affluent countries. Figure 1 shows a bifurcation of our economies. The poorer countries typically had average annual growth rates of per capita GDP greater than 3% per year, while the more affluent economies grew less than 2% annually.

This is not unexpected. It is often thought that poorer countries can experience faster growth than more affluent countries. Following a textbook discussion, we might assume with the Lewis Model: (i) that all economies have access to similar technology, (ii) that poorer countries have generally had lower levels of investment, and (iii) that the marginal productivity of capital declines with higher levels of investment. With these assumptions, if investment can be encouraged in poorer economies by better policies, the impact of this investment on output would be greater than if the investment had occurred in wealthier countries.

Arithmetically, if the relative growth rates of the poorer countries remain higher than seen in the richer countries, the poorer countries would catch up; there would be a convergence of incomes. But how long will this take? I look one generation, or 25 years, into the future and ask what the past growth trajectories will yield, given starting points in 2021. If we run that exercise, we see that only China would catch up to the Japanese standard of living even given a generation of faster growth; the starting gap is too large elsewhere. Except for China and Malaysia, all the other developing countries would be projected to have living standards of less than 30% of the Japanese level.

|

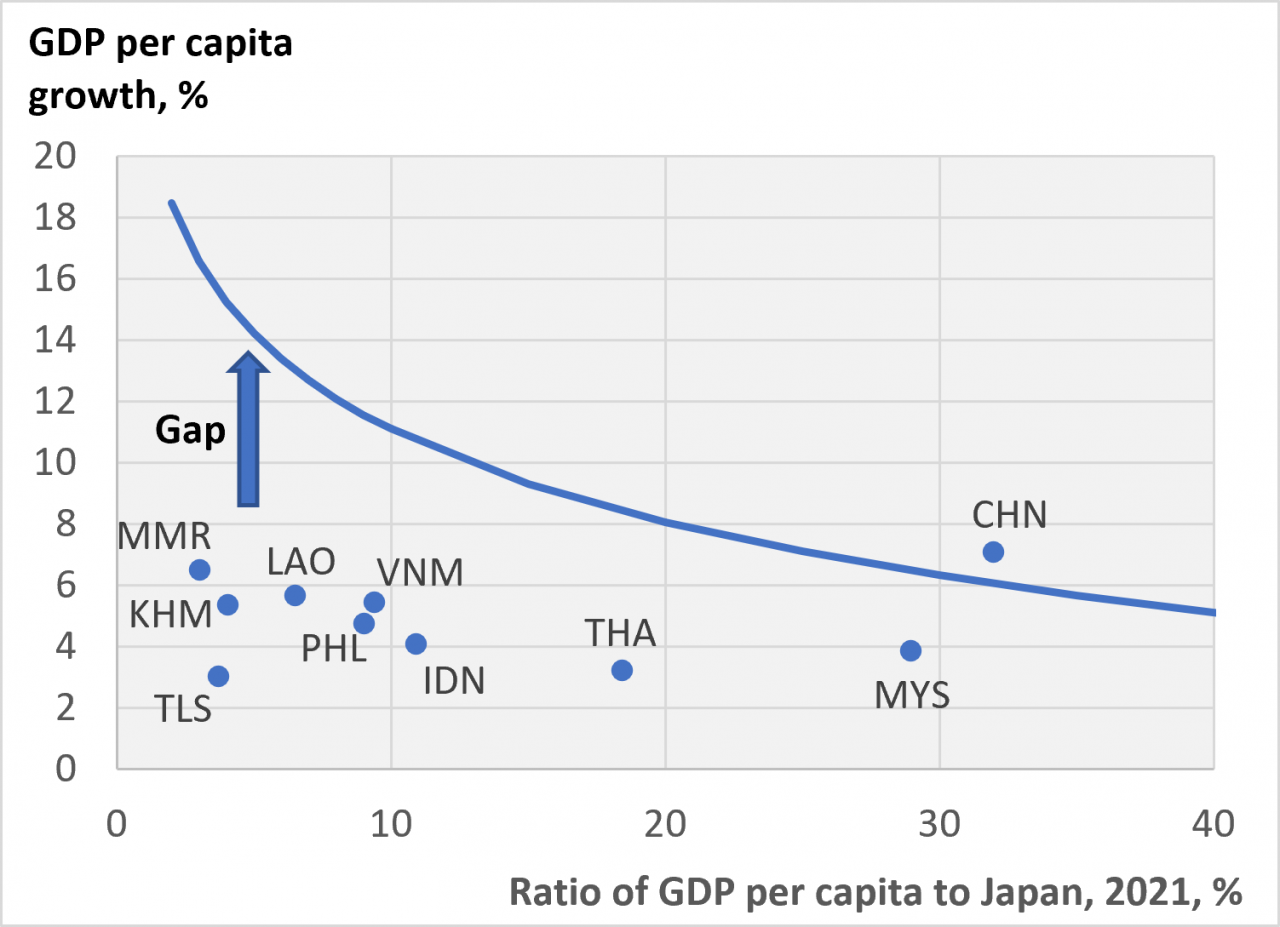

Figure 2: Gap between actual per capita GDP growth and that required to catch Japan by 2046

Data source: World Bank, World Development Indicators. |

Figure 2 provides a visual picture of the challenge. Convergence with Japan will only occur for a restrictive set of starting values of per capita GDP and growth rates, bounded by the curved line. This figure expresses per capita GDP relative to the Japanese value. Thus, if a country started at 20% of the Japanese per capita income in 2021, it would have to grow at 8.1% annually for 25 years to catch up in 2046. The figure shows the large gap that most countries face, except for China and Malaysia, in jumping vertically to the convergence line.

Of course, using different growth rates would give a different picture; however, looking back to the 1960s, while every country has had some good decades, only China consistently showed the growth needed to catch up to Japan over the next generation. The current policy environment in developing Southeast Asia is unlikely to bring about affluent societies—significant income disparities will remain across countries.

This is not a cheerful conclusion. Moreover, our projections may be overly optimistic. Some have argued that growth rates seen in the past will not be seen again. See Rodrik (2012) or Ito (2017). Slower growth in Western markets, for instance, would constrain Asian exports. Moreover, the political climate in Western countries may not support the openness to imports seen in earlier times. The development strategies that worked for some in the past may not work for others tomorrow.

Meeting this challenge will demand efforts in several different directions. At the national level, there needs to be increased attention to the policies that can sustainably increase growth, especially investment in people and infrastructure. However, governments will need to look beyond the policy tools available at the national level. Financial shocks, divergent exchange rates, the impact of COVID-19, climate change, continuing hostility among some governments, and declining fishery stocks are all blockages to growth that need to be addressed at the regional or global level. (Green, 2016) Failure to resolve these problems will seriously constrain growth in Southeast Asia.

When you subscribe to the blog, we will send you an e-mail when there are new updates on the site so you wouldn't miss them.

Subscribe via ![]() in the tool bar.

in the tool bar.

Follow us on social media.

![]()

![]()

Data source: World Bank,

Data source: World Bank,