Has the world passed peak globalization? The prospect doesn't bode well for Emerging East Asia to pursue trade oriented growth. But a three part series on "The Peak Globalization Myth" by Richard Baldwin on VoxEU suggests that broad generalizations about globalization's demise are premature. Findings are: the timing of any peaking differs by region; falling commodity prices have figured significantly in declining trade values; and the future of globalization lies in trade in intermediate services.

This post analyzes trade patterns at the economy level for East Asia with a focus on intra-regional trade and trade in intermediate services to assess prospects. The upshot is that developing regional supply chains and pursuing comparative advantage in intermediate services may offer promising opportunities.

The dynamism of regional supply chains was brought out in a previous post on this blog by Hugot and Platitas. The authors made use of multi-regional input-output data from the Asian Development Bank to show that with the escalation of tensions between the US and China, Asian economies moved toward greater value chain integration within the region. Between 2016 and 2021, trade in intermediate products within Asia more than doubled whereas Asia's trade in intermediates with the rest of the world grew by only about a third.

The analysis of this post makes use of the same multi-regional input-output data to present detail at the level of individual economies. Each input-output table captures trade flows for 35 sectors among 62 economies plus the rest of the world. The framework allows for measurement in value added terms with a distinction drawn between intermediate inputs and final products.

|

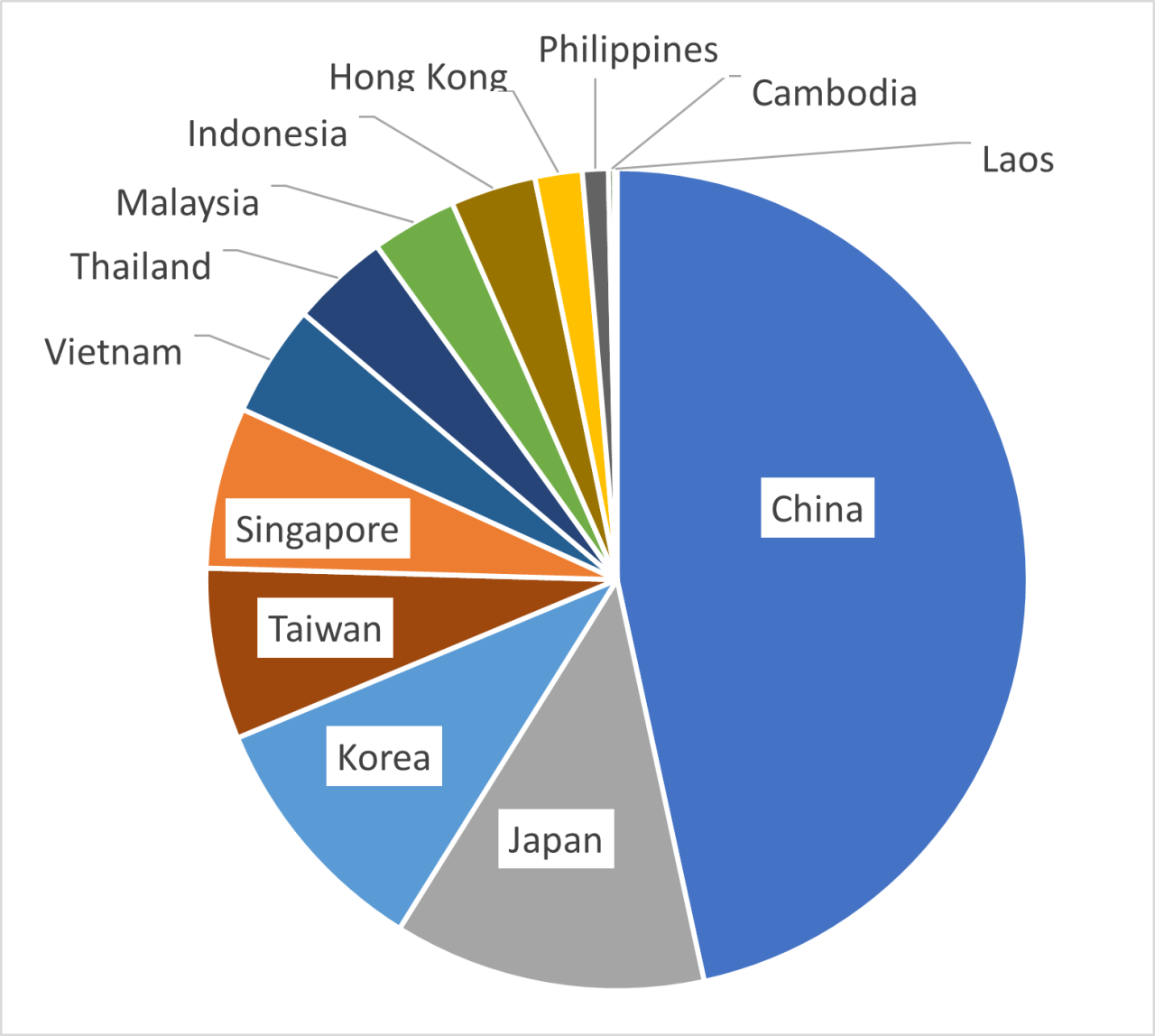

Figure 1. Export Shares in All Products, 2021

Data source: ADB Multiregional Input-Output database. |

China's size gives it a dominant position in East Asian value chains. Figure 1 shows shares in worldwide goods and services exports by economy relative to the region. China accounts for 46.6 percent. Japan follows with 12.3 percent, then Korea with 9.8 percent, Taiwan with 6.7 percent, and Singapore with 6.4 percent. That leaves less than 20 percent for the remaining eight economies combined.

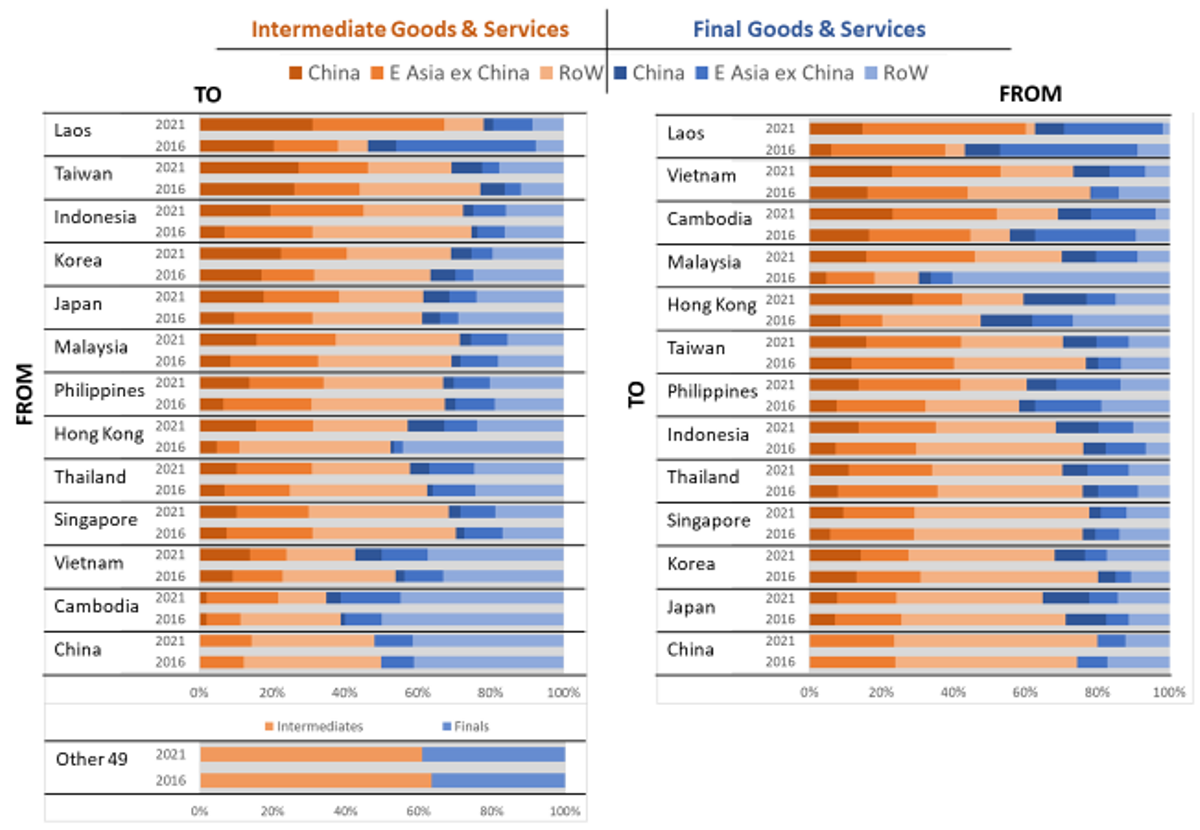

Figure 2 details trade flows by economy. The left panel captures exports from each economy to other blocks, the right panel imports to each economy from other blocks, where the other blocks are China, East Asia excluding China, and the rest of the world. The orange spans represent intermediate goods and services, the blue spans final goods and services. Magnitudes are given for each of 2016 and 2021.

|

Figure 2. Intra-Regional Trade in Intermediate & Final Products, 2016 & 2021

Data source: ADB Multiregional Input-Output database. |

The preponderance of orange indicates that trade in intermediate products has generally outweighed trade in final products. The bands at the lower left provide a benchmark with regard to the other 49 economies in the database. In these economies, too, trade in intermediates predominates, although the share narrowed slightly between 2015 and 2021. For the economies of East Asia, the picture is mixed with respect to the direction of change in intermediate shares overall. However, shares of intermediates trade within the East Asia region increased for most economies, and substantially so for some. This finding echos the result of Hugot and Platitas suggesting that supply chains became more regionalized for East Asia between 2015 and 2021.

Within each panel, economies are ranked by the share of intermediates trade within the region in 2021. Laos tops the list for both exports and imports, not surprisingly given its landlocked geography and small size. China lands at the bottom of the list, also not surprisingly given its large size relative to the region and hence greater need to look outward.

China, Vietnam, and Cambodia have in common export profiles that lean heavily toward final goods versus import profiles that lean toward intermediates. Vietnam and Cambodia thus appear to be following the China model of processing trade, and with a heavy reliance on China and the rest of the East Asian region for their intermediate inputs.

For exports of intermediates to the region, Taiwan places next after Laos with China accounting for a major proportion of its sales. Indonesia also relies heavily on exports of intermediates to the region where, importantly in the Indonesian case, intermediates capture oil and gas.

In a deglobalizing world, regional supply chain development can provide an avenue of opportunity for trade driven growth. That Laos and Cambodia, as two of the least developed economies in East Asia, have forged strong growth in trade in intermediates within the region seems particularly promising given a context of other regional economies also focusing more on building regional supply chains.

|

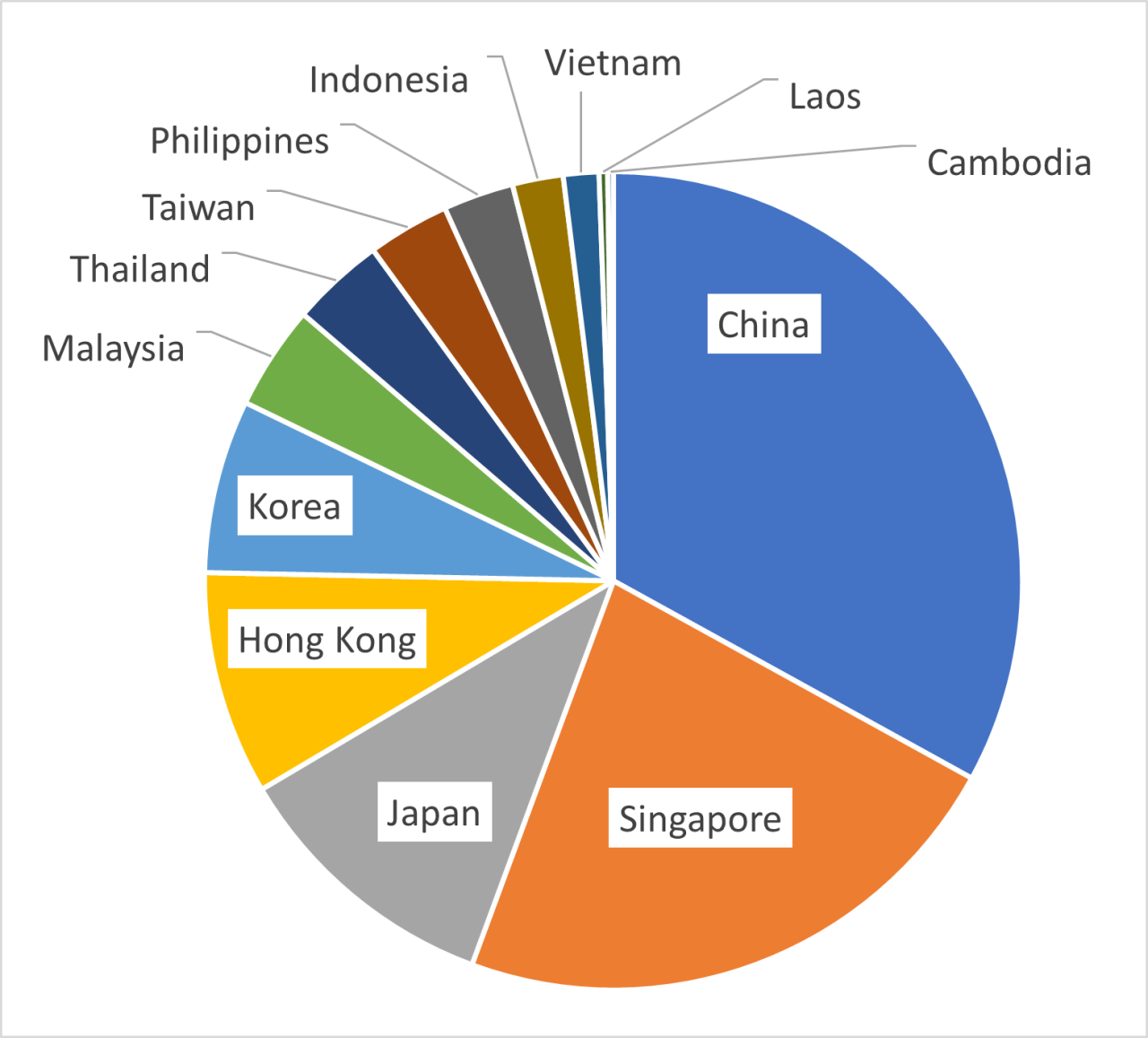

Figure 3. Export Shares in Intermediate Services, 2021

Note: Excludes transport and tourism which continued to suffer the impact of the pandemic in 2021. Data source: ADB Multiregional Input-Output database. |

Another avenue of opportunity for growth, if Baldwin is correct, is intermediate services, whether regionally or globally. Established comparative advantage in this realm is indicated by Figure 3. Export shares for intermediate services diverge significantly from the shares in overall exports shown in Figure 1. China's share shrinks from 46.6 percent to 33.0 percent opening space for other contenders. Most notably, Singapore and Hong Kong take on shares of 22.6 percent and 8.8 percent, respectively. The emphasis on intermediate service exports for these economies is not surprising given their recognized strengths in finance, logistics, and management.

The Philippines also becomes more of a player with its share rising to 2.8 percent from 1.0 percent, putting it in league with Taiwan (3.2 percent) and Thailand (3.7 percent). With trade in intermediate services poised to drive the globalization frontier, the dominance of services that has long been maligned as a weakness in the Philippines (see my review of Fabella on this blog) may become a strength. The Philippines is a global leader in business process outsourcing from a domestic base of operation and its service workers overseas – nurses, seafarers, maids, construction labor – are in wide demand. The time may be opportune to parlay this comparative advantage in services into a force for economic development.

To conclude, insofar as peak globalization applies in any sense at all, it would not seem to preclude East Asia's prospects for trade oriented development. The region shows great dynamism in regional supply chain integration and the potential to exploit comparative advantage in services trade.

When you subscribe to the blog, we will send you an e-mail when there are new updates on the site so you wouldn't miss them.

Subscribe via ![]() in the tool bar.

in the tool bar.

Follow us on social media.

![]()

![]()