The logic is straightforward that policy interventions that seek to break the chain of COVID infection also lower economic activity. Frictions in value creation result from limiting operations for dining and entertainment outlets, curtailing travel, or in general making mobility more stringent. Such disruptions destroy jobs and businesses. Longer term, human and social capital will deteriorate through school closures and reduced business and personal contact . In this reasoning, there is a tradeoff between social safety and economic performance. Call this the stringency effect. The dilemma for policy-making then is a choice between COVID safety and economic prosperity where one comes at a cost to the other.

In reality, however, this tradeoff is offset by an opposing force. Even absent stringency effects, COVID-19 is simultaneously a negative supply shock and a negative demand shock because output will fall from ill health and mortality in the workforce. With heightened concern over COVID, consumption will decline due, for example, to: heightened job insecurity and lowered consumer confidence; increased savings; and lowered propensity to take vacations or eat restaurant meals. Increased risk aversion will depress entrepreneurial activity and reduce investment. In this reasoning, combating the pandemic helps lift economic activity. The higher is social safety, the greater is confidence that life will return to normal, and thus the higher will be economic growth. The correlation here is positive between social protection and economic prosperity. Call this the shock effect.

A further complication over the longer run is that the economy will experience reallocation effects due to efforts to combat COVID: restrictions on mobility and physical clustering harm the travel industry but induce growth and employment in sectors such as those that develop tools for digital engagement, distance working, and telemedicine. As this reallocation proceeds, the same stringency conditions that initially lower economic activity can, instead, spur innovation and growth.

Simply looking at correlations between COVID-19 and economic growth conflates stringency and shock effects as they exert opposing pressures. A more nuanced analysis is needed to disentangle the dynamics.

Empirical Findings

Across all nations, the estimated correlation between COVID safety and economic prosperity is positive but not significantly different from zero. Neither the stringency nor shock effect is dominant. Specifically, measuring COVID-19 performance by the reciprocal of accumulated deaths per million and economic performance by the difference between economic growth rates during 2020-2021 and 2016-2019, the raw Pearson correlation is only 0.09 with a 95% confidence interval of (-0.7, 0.25).

My COVID-19 performance measure assesses how well policy measures and social behaviour have kept COVID-19 mortality low. The higher is this number, the more successful the society has been in combatting COVID-19. My economic performance measure quantifies both the size and direction of the economic shock over the COVID-19 period. The higher this measure of economic performance, the more successful the economy has been. The measure penalizes economies that have historically been fast-growing. Thus, that China’s economic growth over this pandemic period has remained high does not by itself imply success. The important question is: How well did China do compared to how it was doing before the pandemic hit?

Simply focusing on a single correlation, however, shoehorns the analysis into a linear, one-size-fits-all framework.

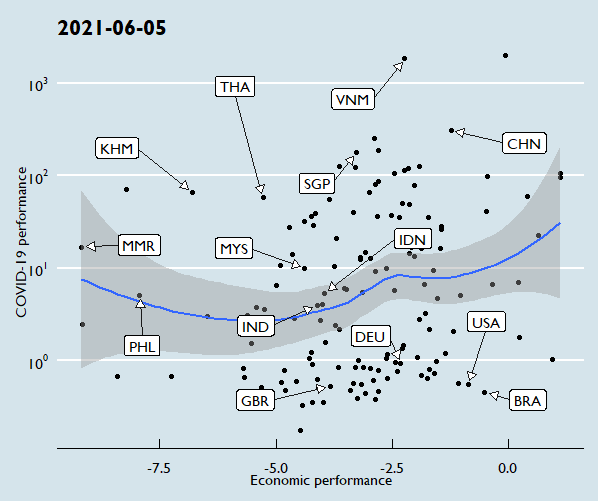

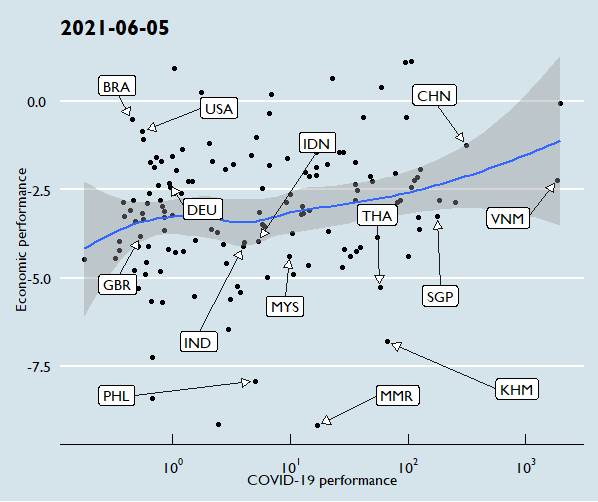

Figures 1 and 2 provide more granular information on the relation between COVID-19 performance and economic performance across nations, the two figures differing in which variable is on which axis.

|

Figure 1: COVID safety conditional on economic performance.

|

|

Figure 2: Economic performance conditional on COVID safety.

Data sources: Our World in Data; IMF WEO database. |

Since the overall correlation is not significantly different from zero, Figures 1 and 2 are expected to show best-fitting nonlinear regression curves that are approximately horizontal on average, although this need not apply throughout. Indeed, Figure 1, which places Economic performance on the horizontal axis, shows on its leftmost portion a small negative slope. But this section of Figure 1 is the only region where the stringency effect manifests to indicate a tradeoff between COVID and economic performance.

Everywhere else in both Figures, the shock effect dominates, meaning confidence in successfully combating the pandemic comes with improved economic performance. Thus, in by far the greater fraction of the space of possible outcomes, preserving public safety lifts, rather than compromises, economic performance.

How have individual nations fared?

The scatterplot shows how individual nations have succeeded or failed relative to average as given by the regression curve.

China appears in the upper portion of both Figures relative to the regression curve. This means that, conditional on its economic performance, China has been more successful than average in preserving social safety. At the same time, conditional on its COVID performance, China has been more successful than average in keeping its economy going.

The US appears in the upper portion in Figure 2, where COVID is on the horizontal axis. Thus, given its COVID performance, the US has kept successful economic growth. However, that the US appears in the lower portion in Figure 1 means it has suffered unexpectedly high COVID deaths given its economic performance.

Like China, Singapore appears in the upper portion of Figure 1: its pandemic safety performance has been above average conditional on its economic performance. In Figure 2, however, Singapore shows up just below the regression line. This is consistent with Singapore’s policy-makers insisting on keeping the economy from excessive recession while, from an abundance of caution, not inducing unnecessary economic expansion that might potentially jeopardise public safety.

To date, both India and Indonesia are approximately on the regression line for both Figures. Cambodia has seen successful COVID safety but with economic performance below average.

The Philippines has kept to an average COVID safety but with a dismal economic outcome. Myanmar appears well to the left in Figure 1 reflecting the double effect of both the COVID shock and the ongoing military coup.

Thailand and Vietnam have had similar experiences. Both appear in the upper portion of Figure 1 meaning they show above average pandemic safety conditional on economic performance. However, both are also in the lower part of Figure 2 meaning conditional on COVID safety performance, they show below average economic results.

Conclusion

Considerable policy discussion has focused on the stringency effect of policy interventions taken against the pandemic. Typically ignored in such debates is the shock effect, where combating the pandemic is good for the economy.

The evidence shows a near-zero correlation between COVID safety and economic performance overall. Large portions of the outcome space however indicate a positive relation. In these regions, the shock effect dominates.

A reasonable conjecture is that stringency effects are large in the short term, but shock effects emerge more gradually over time. In this view, the faster and harder the clampdown, the more likely will the stringency effect be done with and the shock effect then surface.

Statistical Annex

| Economy | ISO3c | Covid | Growth |

| Brazil | BRA | 0.45 | -0.5 |

| China | CHN | 310 | -1.2 |

| Germany | DEU | 0.94 | -2.3 |

| United Kingdom | GBR | 0.53 | -3.8 |

| Indonesia | IDN | 5.32 | -4.0 |

| India | IND | 3.98 | -4.1 |

| Cambodia | KHM | 66.3 | -6.8 |

| Myanmar | MMR | 16.9 | -9.2 |

| Malaysia | MYS | 9.83 | -4.4 |

| Philippines | PHL | 5.04 | -7.9 |

| Singapore | SGP | 177 | -3.3 |

| Thailand | THA | 57.5 | -5.3 |

| United States | USA | 0.55 | -0.9 |

| Vietnam | VNM | 1838 | -2.2 |

When you subscribe to the blog, we will send you an e-mail when there are new updates on the site so you wouldn't miss them.

Subscribe via ![]() in the tool bar.

in the tool bar.

Follow us on social media.

![]()

![]()