Asian economies have been hit differently by the pandemic and have responded differently by way of fiscal and monetary policy. The first post in this series traces differences in economic impact to differences in infection incidence, mobility loss due to transmission mitigation measures, and export decline. This post on fiscal policy and the next on monetary policy look at macro policy responses within the context of policy space.

|

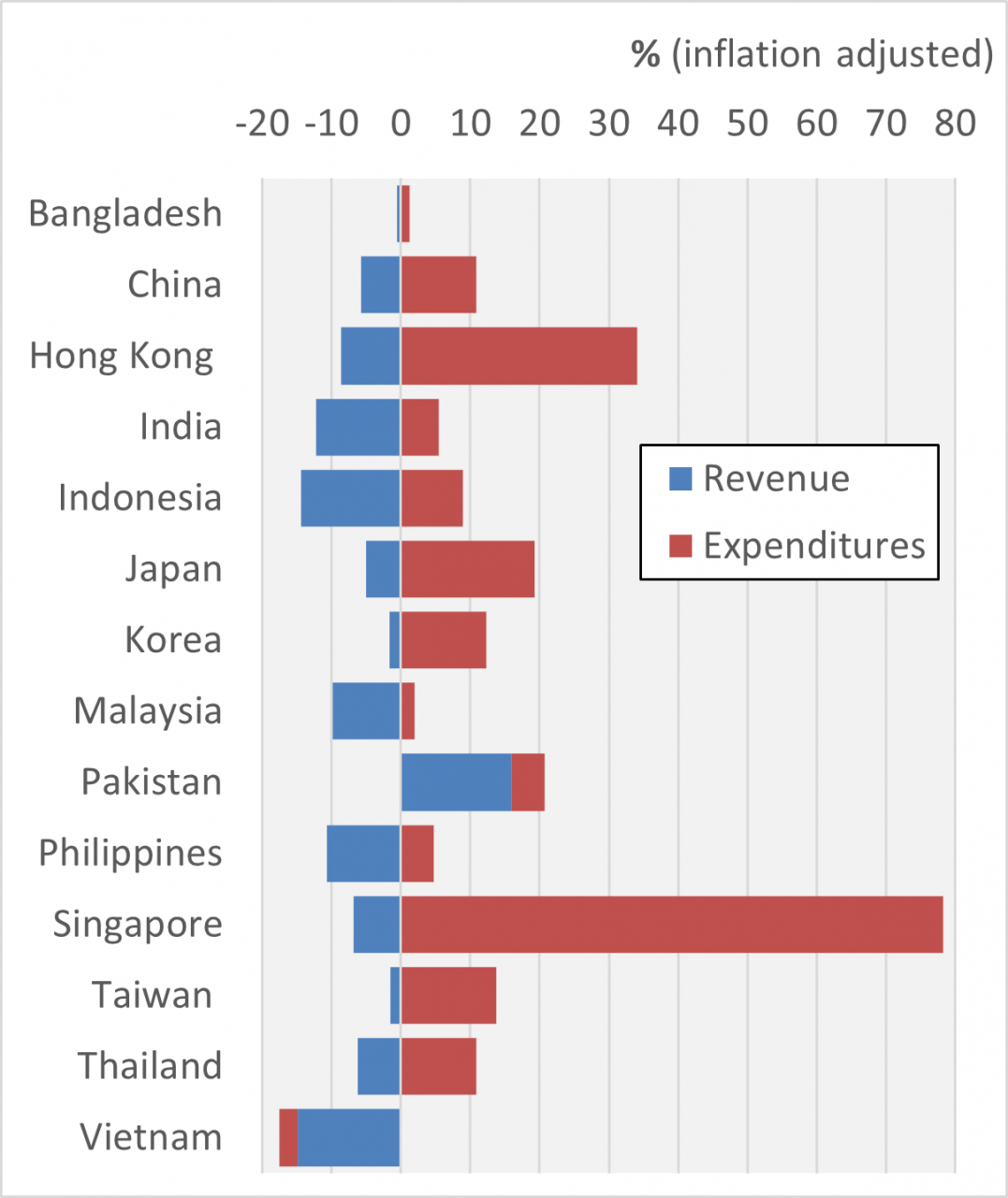

Chart 1:

Data source: IMF Fiscal Monitor |

The pandemic has cried out for increases in government spending to provide public health services; to support households that have lost their livelihoods; and to keep businesses afloat. Against these spending needs, revenues have been undercut by a shrinking tax base. Changes in government revenue and expenditures in 2020 are shown in Chart 1. With the exception of Pakistan, all 14 major Asian economies saw government revenues decline. For India, Indonesia, the Philippines, and Vietnam, the decline was more than 10 percent.

The expenditure picture is more mixed. Singapore stands out for its extraordinary surge in spending. The government implemented five successive budgets in 2020 to raise spending by nearly 80 percent over 2019, or about 20 percent of GDP. The Ministry of Finance credits this fiscal largesse with keeping a bad situation from becoming much worse, its estimates showing that an actual GDP contraction of 5.7 percent would have been larger by 5.5 percentage points without the bold fiscal action. The Singapore government had the luxury of being able to spend freely without regard for borrowing costs given substantial reserve funds accumulated through years of running budgetary surpluses. Moreover, it possesses the administrative capacity to spend effectively at great speed and scale.

How much space a government has to spend in deficit depends on its fiscal sustainability position which is a function of three variables: the real interest rate on borrowing (r); expected real GDP growth (g); and the debt-to-GDP ratio (d). These variables determine the primary balance (pb) that will hold the debt-to-GDP ratio constant (where the primary balance excludes interest payments on debt from the measure of expenditures). If the debt ratio is low initially, some space for it to rise may be incorporated into the reckoning of sustainability. The fiscal sustainability condition is given as:

pb = d(r-g)/(1+g).

A negative value for r–g implies a deficit on the primary balance is permissable under the sustainability condition. The lower the interest rate and the higher the GDP growth rate, the more space the government has for running a primary deficit while still preserving the debt ratio.*

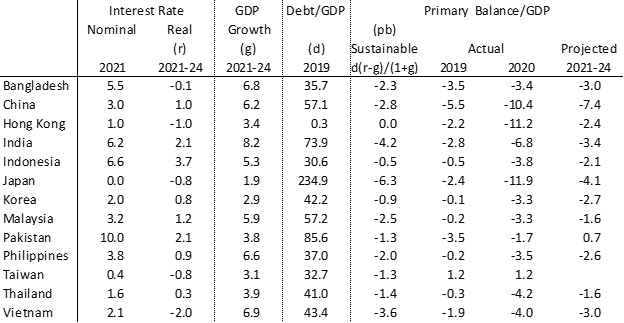

Values of the variables for Asian economies are presented in Table 1. The real interest rate is taken as the nominal rate on 10-year government bonds minus the projected inflation rate for 2021-24. For a few economies (Bangladesh, Hong Kong, Japan, Taiwan, and Vietnam), the real cost of borrowing is negative. Indonesia faces the highest real interest rate, a key reason being its heavy reliance on foreign creditors. Promising growth projections (per the IMF) give greatest advantage to India, Vietnam, the Philippines, Bangladesh, and China.

|

Table 1: Fiscal Space Determinants & Utilization, 2019-24

Data sources: Nominal interest rates, World Government Bonds; Taiwan primary balance, Republic of China Ministry of Finance and author calculations; all else, IMF DataMapper. |

Before the pandemic, reported debt-to-GDP ratios lay at the margin of concern for Pakistan, at 85.6 percent, and India, at 73.9 percent. Japan's stratospheric debt ratio has long proven tolerable with costs of funding remaining low due to ample domestic savings. For some economies, a caveat is that reported figures exclude off-budget spending (e.g., subsidies to money losing state enterprises) and contingent liabilities (e.g., pension obligations or prospective bailouts of failing financial institutions). With an eye to these considerations, debt ratios in China and Malaysia become more worrisome. All other economies have space for their debt ratios to rise by standard benchmarks.

Hong Kong is essentially unconstrained in its spending given negligible prior debt. Authorities took advantage of this latitude in 2020 to ramp up the primary deficit to 11.2 percent of GDP on expenditure increases of 34 percent relative to 2019 (Chart 1), second only to Singapore (for which budget details are not publicly available). Taiwan alone ran a primary surplus in 2020, maintaining a stable budget balance relative to GDP, evidence of the mild consequences of the pandemic there. Pakistan managed to reduce its deficit in 2020 while Bangladesh held its deficit roughly constant. In all other cases, primary deficits increased within a range of 2-5 percentage points of GDP. Moreover, in all cases but Taiwan, primary budget deficits in 2020 exceeded the sustainability threshold meaning debt-to-GDP ratios would have risen. Projections by the IMF show these enlarged deficits to be temporary, with most budgets settling back toward sustainable levels within a few years, China being a noteworthy exception with the largest sustained gap.

A global emergency on a scale beyond living memory presents great pressure for governments to take on additional debt. Good fiscal management in normal times can ensure a comfortable space for this. The sudden decline in revenues caused by the pandemic is particularly difficult to weather without recourse to borrowing if performance of essential government functions is to continue. In addition, the pandemic necessitates increases in public health expenditures if the disease is to be conquered. Beyond these imperatives, public support for sustaining businesses and livelihoods through the upheaval of the crisis can mitigate scarring and smooth the way to eventual recovery. For most Asian economies though, room to maneuver is limited.

_______________________

*A previous post reviews a webinar discussion between Olivier Blanchard and Arvind Subramanian of the implications of this fiscal sustainability condition for policy in advanced versus developing countries.

This post is adapted from Chapter 15 of Macroeconomics for Emerging East Asia (Cambridge University Press, 2022; RePEc).

See also:

Economics of the Pandemic (Part I): Covid Cases, Mobility Loss, and Exports

Economics of the Pandemic (Part III): Monetary Policy

When you subscribe to the blog, we will send you an e-mail when there are new updates on the site so you wouldn't miss them.

Subscribe via ![]() in the tool bar.

in the tool bar.

Follow us on social media.

![]()

![]()