The 'new fiscal consensus' holds that major advanced economies have the fiscal space to go big on stimulus and should do so in response to the pandemic. In a recent webinar sponsored by the Ashoka Centre for Economic Policy in Haryana, India, Olivier Blanchard made the case for the new fiscal consensus and Arvind Subramanian then responded on the relevance for emerging market economies such as India. This post extends elements of their analysis to the major emerging economies of Southeast Asia: Indonesia; Malaysia; the Philippines; Thailand; and Vietnam.

Blanchard explained that to preserve a stable debt/GDP ratio, the following condition must hold:

s = (r-g)/(1+g) d

where s is the surplus relative to GDP on the primary fiscal balance which excludes interest payments on debt; r is the real interest rate; g is the real GDP growth rate; and d is the debt/GDP ratio. If r>g, then the primary balance must be positive to cover interest payments on debt while preserving the debt ratio. Conversely, if r<g, the government can borrow to fund current spending to the extent of the term on the right-hand side without accumulating debt relative to GDP. The latter (r<g) represents the extraordinarily fortuitous circumstance major advanced economies find themselves in and they should take advantage of it.

Subramanian responded that emerging economies must be more cautious in applying this fiscal arithmetic, despite the fact that r<g pertains as much or more so. In the case of India, r-g has been negative for the last decade – the value reaching as low as -12% – and the primary deficit has been small at around -3%, yet between 2014 and 2019, the debt/GDP ratio rose from 66.5% to 72.4%. The slippage in the fiscal math is attributed by Subramanian to contingent liabilities (bailouts of the financial system and other off-balance sheet obligations) such that "the standard analysis can overstate the room for fiscal policy." (52:20) Moreover, interest rates on government debt tend to be more volatile in emerging economies, especially when foreign creditors are involved, and the government budget is less able to absorb rising interest costs. India's scope for fiscal stimulus in response to the pandemic is thus more limited than the application of Blanchard's fiscal math would suggest.

Let us consider the situation in Southeast Asia with respect to the fiscal math. Key indicators are laid out in Table 1. The interest rate on government borrowing differs appreciably among the five countries, where the nominal rate is given by the current yield on ten-year government bonds and the real rate is derived from inflation projections for 2020-3. Vietnam's relatively high inflation of about 4% confers a negative real rate of -1.3%. Thailand and the Philippines enjoy real rates near zero while Malaysia and Indonesia face rates of 1.4% and 3.7%, respectively. Growth rate projections for 2020-3 range from 1.4% for Thailand to 5.7% for Vietnam. The resulting difference r-g is negative for all but Indonesia, for which it is zero, with Vietnam an outlier at -7.1%. The math thus has it that all but Indonesia are in a position to run primary deficits while still maintaining stable debt/GDP ratios.

Table 1: Fiscal Indicators (%)

|

Interest Rate Nominal Real (r) |

GDP growth (g) |

r-g |

Primary balance /GDP (s) |

Debt /GDP (d) |

Interest expense /Revenue |

||||

| 2021 | 2020-3 | 2020-3 | 2020-3 | 2019 | 2020 | 2021-3 | 2020 | 2019 | |

| Indonesia | 6.1 | 3.7 | 3.8 | 0.0 | -0.5 | -4.5 | -2.2 | 38.5 | 12.2 |

| Malaysia | 2.7 | 1.4 | 3.4 | -1.9 | -1.7 | -4.0 | -1.6 | 67.6 | 12.5 |

| Philippines | 3.0 | 0.0 | 3.0 | -3.0 | -0.2 | -6.0 | -4.0 | 48.9 | 11.5 |

| Thailand | 1.4 | 0.3 | 1.4 | -1.1 | -0.3 | -4.8 | -2.1 | 50.4 | 5.9 |

| Vietnam | 2.4 | -1.3 | 5.7 | -7.1 | -1.9 | -4.6 | -3.1 | 46.6 | na |

Data Sources: Nominal interest rate is from ADB Asian Bonds Online. Interest expense /Revenue is from IMF Government Financial Statistics. All others are from IMF DataMapper.

In fact, all five countries were already running primary deficits in 2019, and the margins increased sharply in 2020 with the pandemic. For the Philippines, the primary balance stood at -6.0% in 2020 while for others it was in the -4% to -5% range. Looking ahead to 2021-3, primary balances are projected to remain below a 2019 benchmark for all but Malaysia, most substantially so for the Philippines. By the r-g measure of fiscal space then, Southeast Asian countries are not crimping on running deficits.

The existing stock of debt relative to GDP also factors into the calculation of fiscal space. A previous post has examined the history of government debt in East Asia with implications drawn for fiscal response to the pandemic. Table 1 above captures the ratio for 2020. Malaysia has the highest ratio at 67.6%, with this ratio having tracked upward in recent years. Although Indonesia's debt ratio appears low at 38.6%, the high interest rate incurred on public debt evinces the country's difficulty raising funds and indeed Indonesia relies to a greater extent than the others on foreign creditors. Debt ratios for the remaining three at 50% or less, and having trended downward in recent years, affirm a sense of space to step up borrowing.

Subramanian advised that we also look at annual interest expense relative to government revenue, shown in the last column of Table 1. This ratio gives a perspective on borrowing space relative to government capacity to service additional debt. In India's case, the ratio is over 21% in contrast to 13% for the US and 7% for the UK. By these benchmarks, ratios in the 11.5-12.5% range for Indonesia, Malaysia, and the Philippines seem manageable while a ratio of 5.9% for Thailand leaves room to spare. Of course, if interest expense within the government budget rises faster than GDP, either revenue/GDP must be increased or other expenditures/GDP will have to be cut.

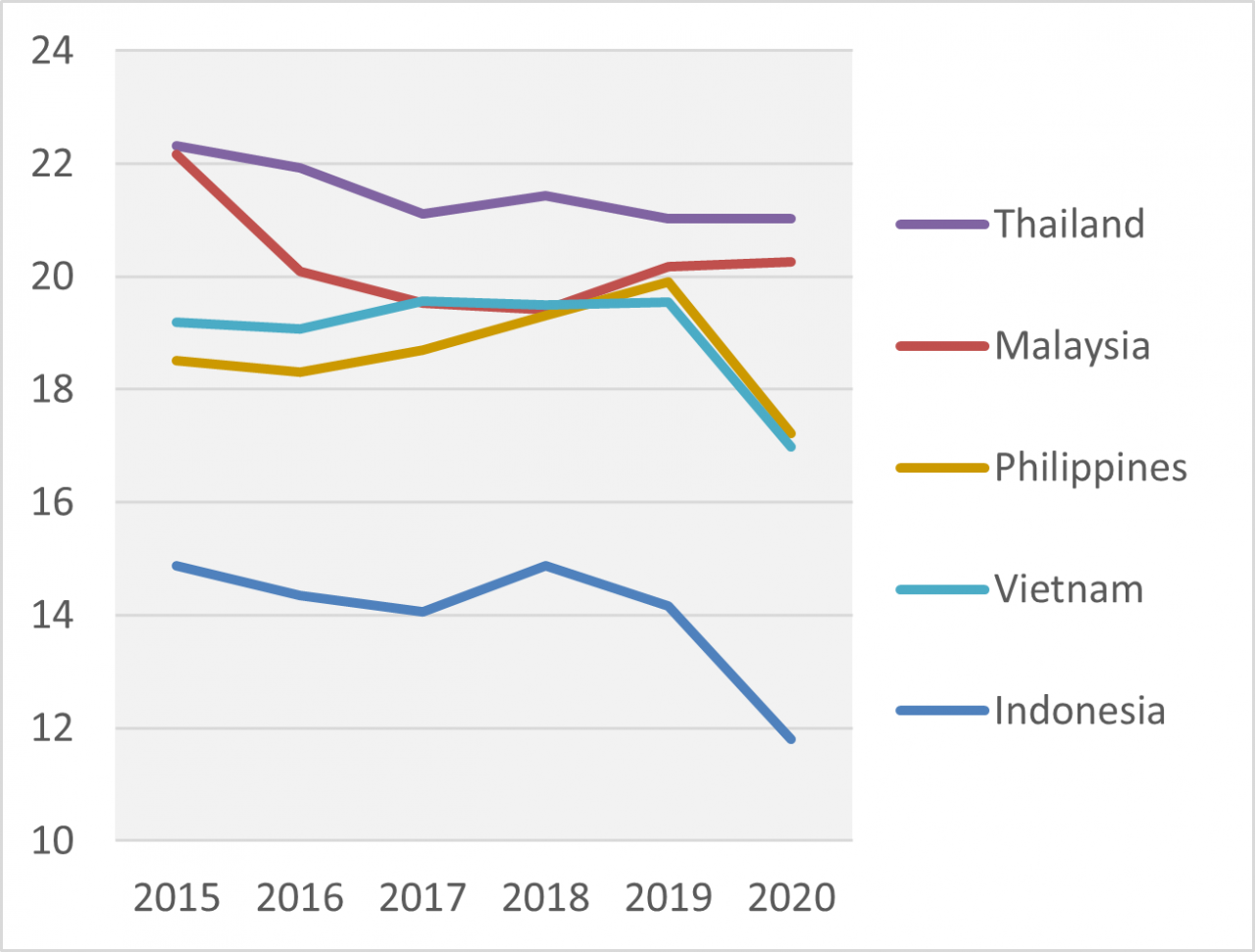

|

Figure 1: Government Revenue /GDP (%)

Data Source: IMF DataMapper |

With that, we are motivated to look at the impact of the pandemic on government revenue, shown in Figure 1. Experiences diverge starkly across the five countries. Thailand and Malaysia are managing to sustain stable revenue/GDP ratios even as the Philippines, Vietnam, and Indonesia have seen their ratios drop by more than 2 percentage points. For the latter three then, increases in borrowing have gone largely to make up for revenue shortfalls rather than to meet public health and welfare needs arising from the pandemic. Indonesia stands out for an exceptionally low ratio of government revenue/GDP which weighs on its ability to service debt and factors into its high cost of borrowing.

Blanchard and Subramanian have helped frame the decision making calculus as to how much debt governments should take on to fight the pandemic and shore up their economies. The calculus is made more complex by the dynamics of the interaction between government spending now and revenue in the future. Failure to keep businesses afloat in the short term will undermine recovery for years to come and thus compromise fiscal sustainability perhaps more than borrowing now to try to stay the course. Long term, the important lesson to be taken is that marshalling fiscal space in good times is the best hedge against crisis in the event of severe shock.

Final note: much is hard to measure in emerging economies, but government debt and associated obligations are not. Blanchard makes light of default, but this too probably deserves more caution. Serious scrutiny is focused on sovereign creditworthiness in emerging economies.

__________________________

Related post: East Asia's Fiscal Response to Crisis, Then & Now, 14 August 2020

When you subscribe to the blog, we will send you an e-mail when there are new updates on the site so you wouldn't miss them.

Subscribe via ![]() in the tool bar.

in the tool bar.

Follow us on social media.

![]()

![]()